Charlotte Mid-Year Economic Outlook

A capital-led expansion positions the Queen City to outperform peer Sun Belt metros through 2030

Download PDF versionExecutive Summary

The U.S. economy continues to display surprising resilience amid heightened uncertainty surrounding higher energy and raw materials prices emanating from the Iran War. Hiring has clearly slowed, and consumers have become more selective about discretionary purchases. Underlying demand, however, remains intact, with real final sales to private domestic users rising at around a 2.5% annual rate. Capital spending is carrying this part of the cycle. Private fixed investment in AI infrastructure, power generation, advanced manufacturing, aerospace and defense, and life sciences continues to drive output even as firms produce more with fewer workers. The result is a productivity-led, job-light expansion, not a shock-driven cyclical retrenchment, and Charlotte seems purpose-built for it.

The Queen City's depth in financial services, its energy and infrastructure advantages, its logistics connectivity, its expanding technology and life sciences ecosystem, and its abundant land and water resources line up exceptionally well with a capital-heavy, productivity-driven cycle. Even as hiring has slowed nationally and across peer Sun Belt metros, Charlotte continues to add jobs and to attract major capital commitments. The job-growth pace has stepped down materially from the preliminary readings reported through late 2025, but Charlotte still outperforms most Sun Belt peers.

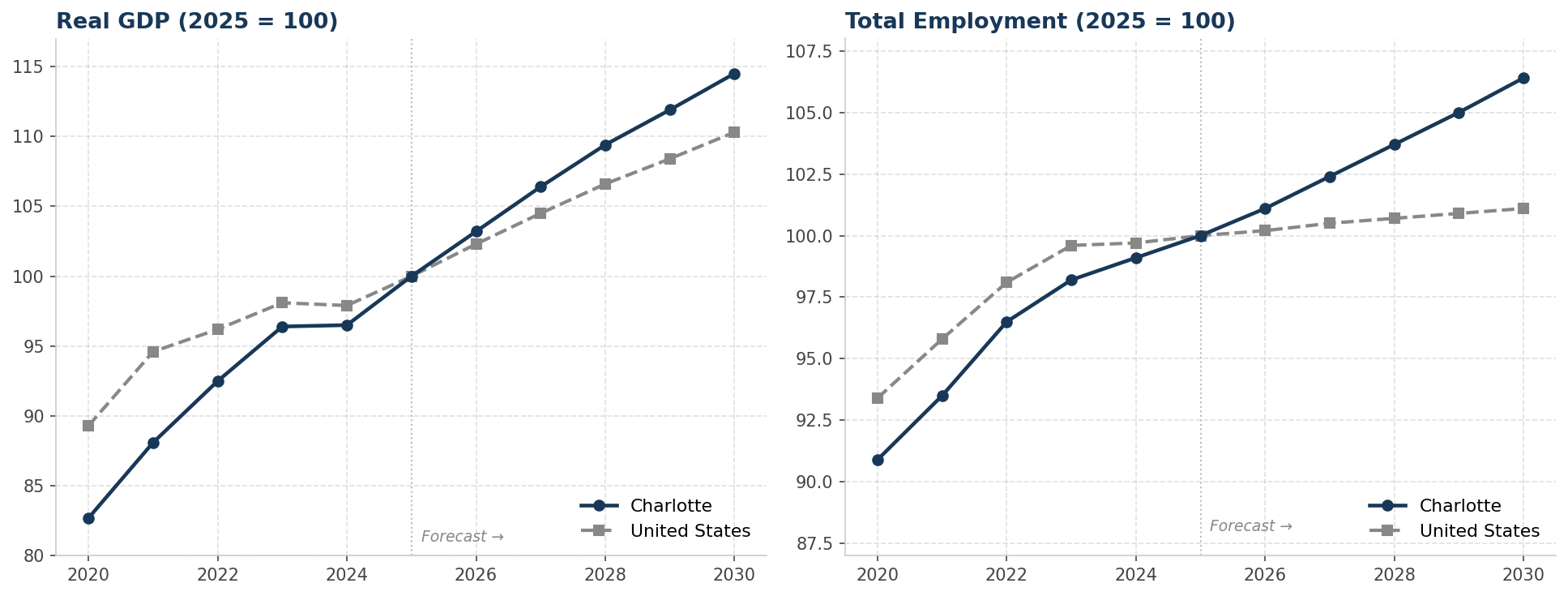

Our base case calls for Charlotte real GDP growth of 3.2 percent in 2026 and an average 2.8 to 3.0 percent annually through 2030, comfortably above the projected 2.3 percent U.S. pace. The risks are real. Housing affordability is the most-cited concern, and three major infrastructure and development decisions reaching critical milestones this year (detailed below) together represent the most consequential test of Charlotte's collaborative public-private machinery in a generation. The underlying diversified base provides a meaningful buffer that did not exist a decade ago, but the metro's competitive edge has never come from any single asset. It has come from the willingness of business, labor, and government to find common ground and act.

Key Takeaways

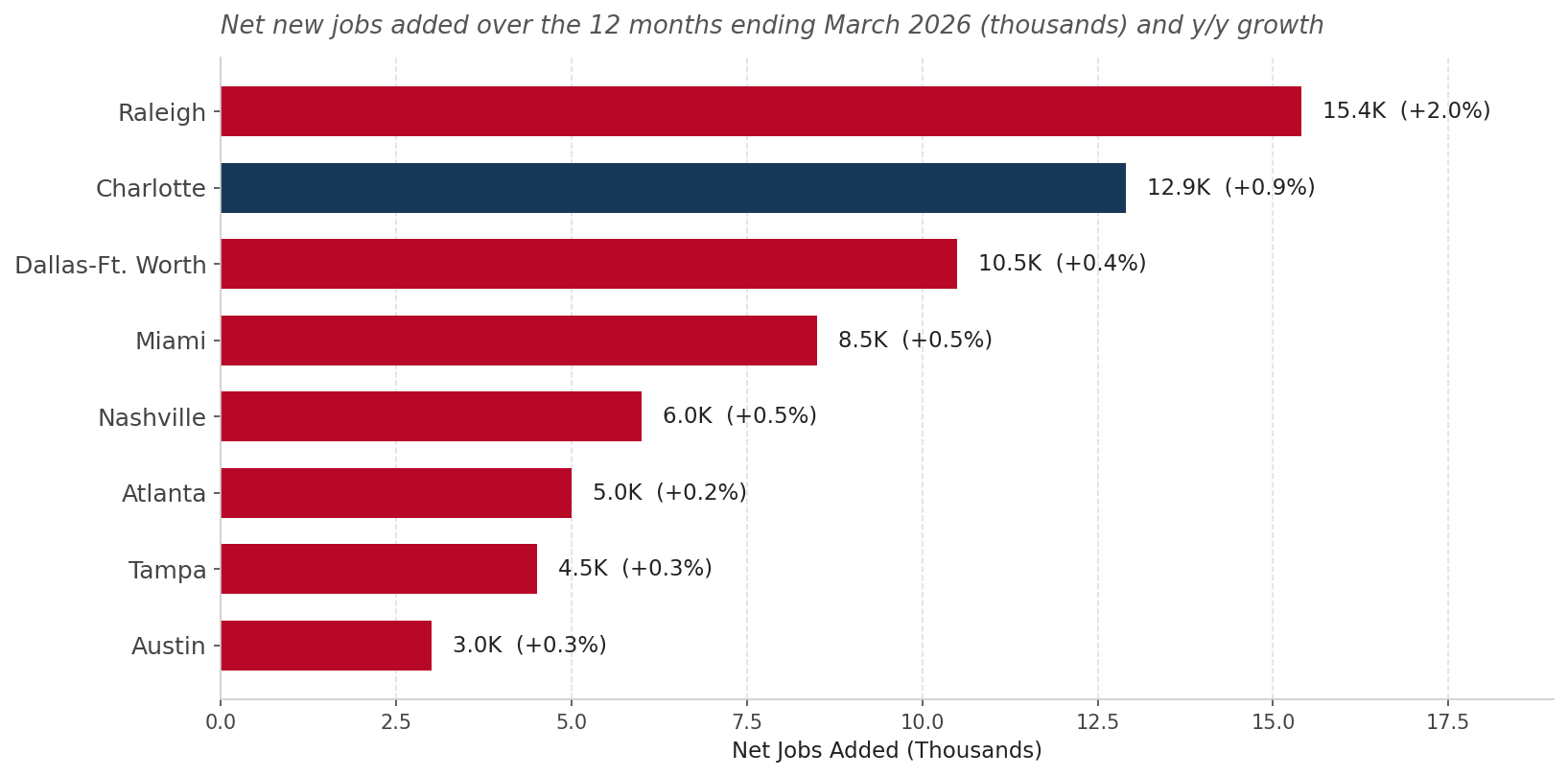

- Charlotte added 12,900 net new jobs over the trailing 12 months, a 0.9% gain — well below the preliminary 2.7% figure that prevailed before the annual benchmark revision, but still ahead of most Sun Belt peers. Separately, the city of Charlotte added more new residents (+20,731) than any U.S. city in the latest Census estimates (July 2024 to July 2025).

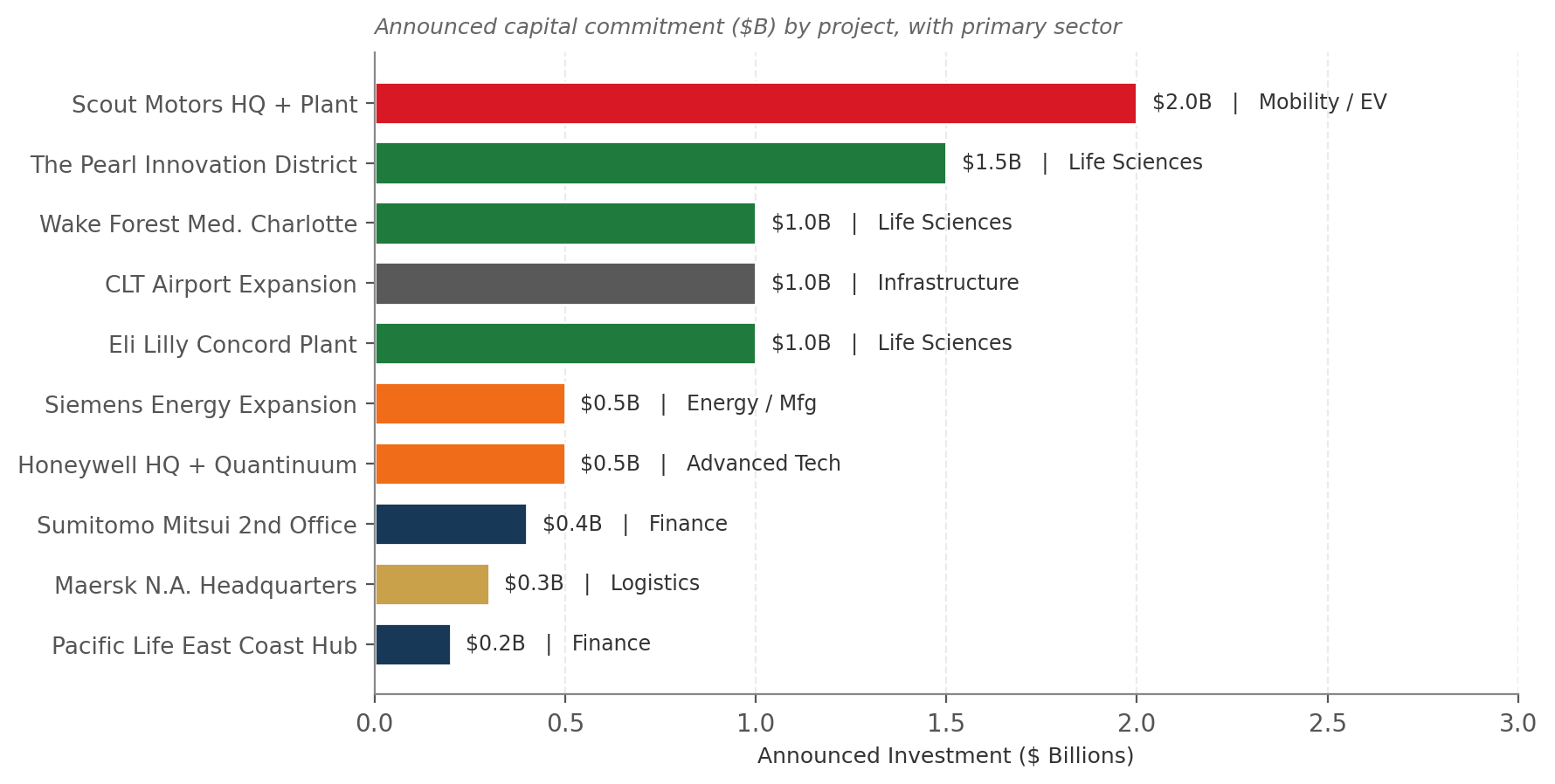

- Recent capital announcements span every key sector: Scout Motors (U.S. HQ in Plaza Midwood), Sumitomo Mitsui (second office, +2,000 jobs), Pacific Life (East Coast hub in South End), Maersk (North American HQ), Siemens Energy (gas turbine expansion), and The Pearl innovation district. Total committed capital exceeds $10 billion.

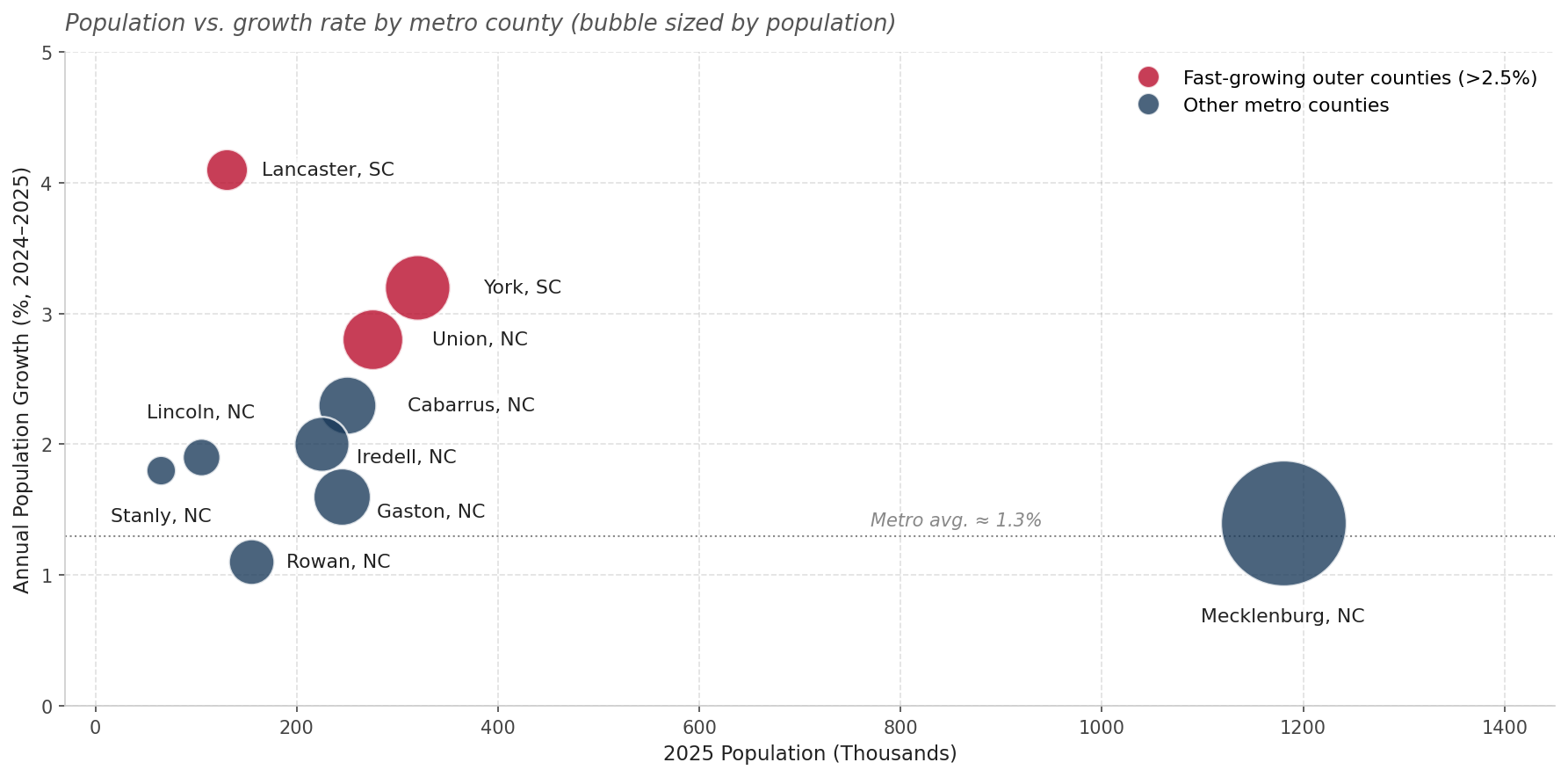

- Growth is now most rapid in the metro's South Carolina counties — Lancaster (+4.1%) and York (+3.2%) — reinforcing Charlotte's role as a regional hub. The completion of I-485 beltway in 2015 unlocked vast tracts of suburban land both within the city and outlying areas just as Sun Belt migration accelerated, providing a housing supply safety valve few peer metros enjoy.

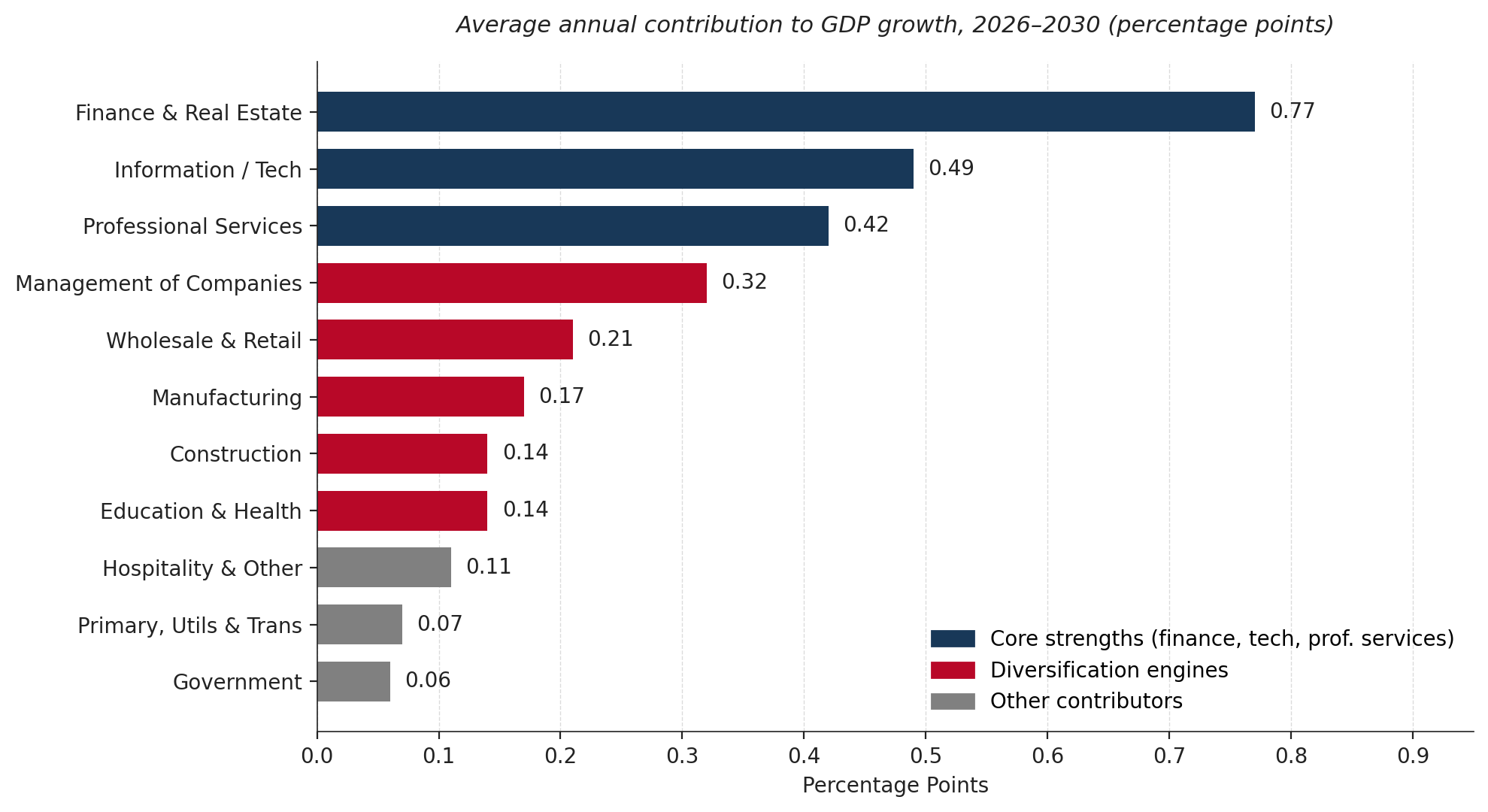

- Real GDP is projected to grow 3.2% in 2026 and average 2.8% to 3.0% annually through 2030, comfortably above the projected 2.3% U.S. pace. Finance and insurance remains the lead driver, with technology, professional services, life sciences, advanced manufacturing and logistics providing meaningful diversification.

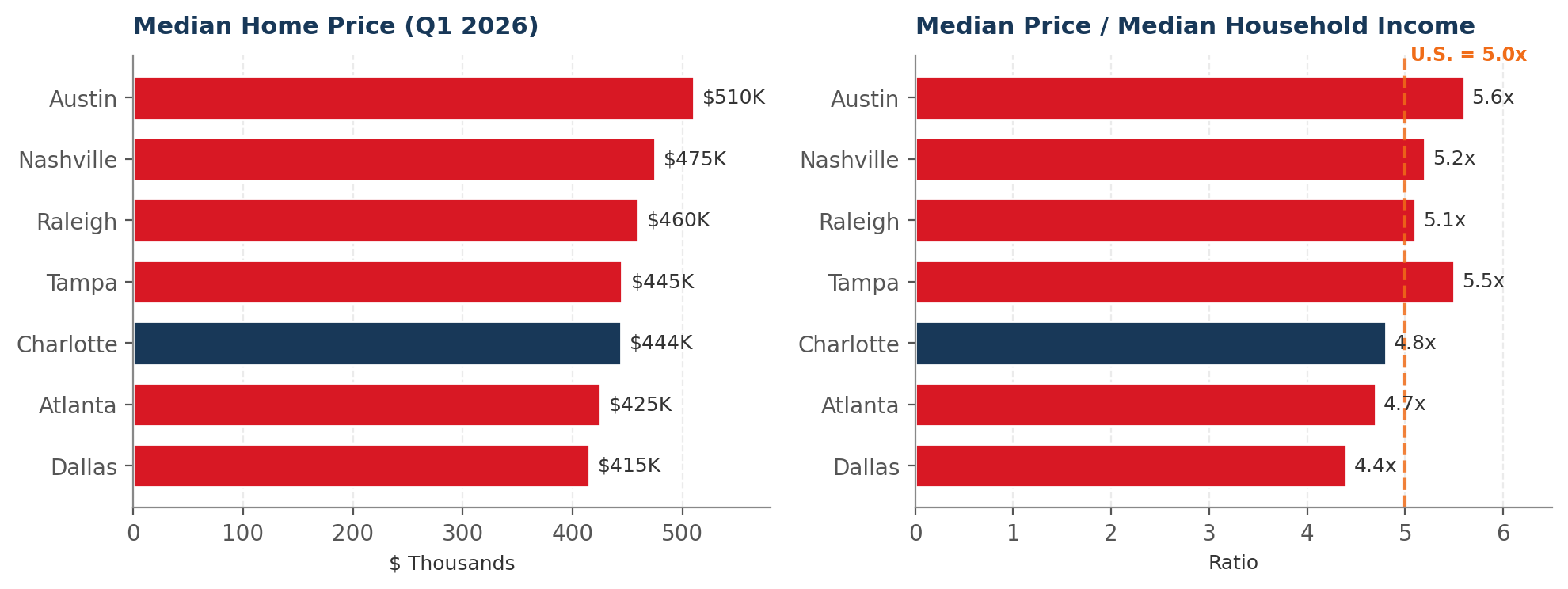

- Housing affordability remains Charlotte's largest single risk, but the metro still holds a real edge, with homes priced 4.8x median household income vs. 5.6x in Austin and 5.5x in Tampa. Preserving that edge through continued supply growth in outer-ring counties and along the LYNX corridors is essential to sustaining migration momentum.

- Three infrastructure tests will shape Charlotte's next decade: I-77 South (City Council and CRTPO rescinded support in May, and NCDOT will withdraw roughly $700 million in committed state funding), the Airline Use and Lease Agreement (extended one year in May while a successor deal is negotiated), and Brooklyn Village (master developer Peebles lost control of the first-phase parcels in a May foreclosure; the county had already halted negotiations last August). All three are tests of the public-private collaboration that built modern Charlotte.

Section 1: A Capital-Led Cycle Plays to Charlotte's Strengths

Beneath the headline numbers, something important is happening in Charlotte's economy. Revised data show that job growth moderated meaningfully in late 2025, with the metro adding roughly 12,900 net new jobs over the trailing twelve months ending March 2026, a 0.9 percent gain. That is a step down from the preliminary figures that prevailed before the benchmark revision, but it remains stronger than the gains reported for most peer Sun Belt metros. More importantly, the moderation in hiring has not been accompanied by a slowdown in capital deployment. Announced investment in headquarters operations, advanced manufacturing, life sciences, logistics and energy continues to accelerate, even as firms find ways to do more with the workforce they have. Charlotte is now one of the clearest examples of the broader national pattern: capital-led, productivity-driven growth that is increasingly light on jobs.

The divergence reflects the metro's particular industrial mix. Finance and insurance has been a key contributor, with selective hiring and faster GDP growth driven by technology investment and operational scaling. The headquarters category, what the BEA calls "management of companies," has continued to add positions selectively. Both sectors are investing in technology, scaling operations, and adding selectively in high-productivity functions.

Manufacturing tells a similar but slightly different story. Employment in the sector has slipped, but GDP is forecast to grow 1.7 percent annually through 2030 as the region's diversified industrial base deepens capital intensity and automation. That base is broader than commonly understood. Mecklenburg County alone is home to approximately 800 manufacturing plants and one of the largest manufacturing workforces of any North Carolina county.

Charlotte also has a growing roster of manufacturers headquartered in the region. Honeywell relocated its corporate headquarters from New Jersey in 2019, joining Corning's optical communications division headquarters in Charlotte, which relocated from neighboring Hickory and anchors a fiber-optic cable manufacturing footprint that extends throughout the greater Charlotte area. The firm recently announced a $6 billion Meta supply agreement that will make one of its Hickory plants the world's largest fiber-optic cable facility. The headquarters cluster also includes several Charlotte-rooted manufacturers that have grown into national franchises: Nucor, the largest steel producer in the United States and North America's largest recycler; Coca-Cola Consolidated, the country's largest independent Coca-Cola bottler with roughly 17,000 employees and eleven manufacturing facilities serving fourteen states; and privately held Charlotte Pipe and Foundry, the nation's leading maker of cast iron and plastic plumbing pipe, which completed the relocation of its century-old foundry to a $460 million greenfield plant in Oakboro in 2023, freeing the 55-acre Uptown site for the Iron District redevelopment now breaking ground along the planned Silver Line corridor.

The supporting base extends well beyond Mecklenburg. Gaston County retains roughly 16,000 manufacturing jobs, anchored by industrial machinery, advanced materials, and a textile sector that has reinvented itself around technical and specialty fabrics. Major employers include Daimler Truck North America, Parkdale Mills, Stabilus, WIX Filtration and Curtiss-Wright.

York County's industrial base is led by Schaeffler's automotive components operation in Fort Mill, the county's largest manufacturer with roughly 950 employees, alongside a growing roster of German, Swedish, and Norwegian advanced manufacturers including Coroplast, Atlas Copco, and Elkem Silicones.

Manufacturing also makes an important contribution in Union County, where 195 manufacturing firms employ roughly 14,800 people, anchored by an aerospace cluster of about 4,500 jobs built around ATI's high-performance alloy operation in Monroe, alongside Collins Aerospace, Greene Tweed, and Icon Aerospace. Tyson Foods and Pilgrim's Pride lead a substantial food processing base, and recent arrivals like chemical manufacturer Dymax ($46.7 million, 227 jobs) reflect continued momentum.

Section 2: The Capital Investment Pipeline

Recent capital announcements illustrate the breadth of momentum. Sumitomo Mitsui Banking Corp. is opening what is essentially a second U.S. headquarters operation in Charlotte with plans to add roughly 2,000 jobs. The firm subleased 194,000 square feet at 301 South College Street in Uptown, the former headquarters building for Wachovia and First Union prior to that. Pacific Life announced in late 2025 that it will establish a new East Coast hub in South End, adding about 300 positions in finance, actuarial, and technology roles. Maersk selected Charlotte in late 2025 as its North American headquarters, expanding local employment to more than 1,300, and Scout Motors announced it will locate its U.S. headquarters in Charlotte's Plaza Midwood area alongside its Blythewood, South Carolina assembly plant currently under construction and scheduled to begin production in 2027 approximately 75 miles south of Charlotte.

Advanced manufacturing and energy provide important diversification. Siemens Energy is expanding its gas turbine operations to meet surging demand from data center operators, including Google's Caldwell County build-out, seeking alternative power sources, and the supplier ecosystem around it continues to thicken. Apple maintains one of its largest data center complexes nearby, outside Hickory, and Meta and Amazon operate or are building large facilities in the region. Berlin-based Trench Group, which spun out of Siemens Energy in 2024, broke ground in August 2025 on a $50 million plant for its HSP US subsidiary just down the road from Siemens Energy's southwest Charlotte site, where it will manufacture high-voltage transformer bushings beginning in early 2026. AVL Manufacturing, a Hamilton, Ontario-based maker of industrial generator enclosures used for data center backup power, separately announced a $56 million, 232,000-square-foot first U.S. plant in Charlotte's Steele Creek area that will add more than 325 jobs. On the life sciences side, German family-owned Groninger USA, the U.S. headquarters of a leading manufacturer of pharmaceutical and consumer-health filling machines, is investing $15.1 million to expand its Steele Creek operation and add 60 engineering and production positions to a workforce that will reach 172. The startup and technology ecosystem is broadening well beyond its historic dependence on the financial base. Fintech remains strong, but healthcare, life sciences, MedTech (bolstered by The Pearl innovation district and the new Wake Forest School of Medicine campus), and logistics and B2B software are all gaining real traction.

The most concentrated expression of this advanced-manufacturing thesis is taking shape twenty miles northeast of Uptown at The Grounds at Concord, the 500-acre former Philip Morris cigarette plant that closed in 2010 and is now being recycled into one of the Southeast's largest advanced manufacturing campuses. Eli Lilly opened a 1.3-million-square-foot injectables facility there in June 2024 to produce its GLP-1 diabetes and obesity drugs Mounjaro and Zepbound, doubling its initial investment to $2 billion during construction and creating roughly 600 jobs at full capacity. Adjacent to the Lilly campus, an Austrian-led consortium of Red Bull, Rauch Fruchtsäfte, and Colorado-based Ball Corporation broke ground in September 2025 on a $1.5 billion, 2.3-million-square-foot integrated beverage manufacturing and distribution complex that will fill three billion cans annually at peak buildout in 2031 and add another 700 jobs. Carvana already operates an inspection and reconditioning facility on the site. The Concord cluster provides one of the clearest examples of how Charlotte's economy is not simply growing but constantly reinventing itself. The textile, apparel, furniture, and tobacco industries that defined the regional economy for most of the twentieth century have receded, and faster-growing industries — life sciences, beverages, advanced manufacturing, energy infrastructure, and logistics — are taking their place, often on the same land and drawing on the same labor pool. More than $3.5 billion has been committed to a single former cigarette plant in less than four years, and the buildout still has room to run.

Underpinning all of this is Charlotte Douglas International Airport, which served 53.6 million passengers in 2025, its second-busiest year on record, and now ranks seventh in the world by aircraft operations. CLT offers nonstop service to 194 destinations, more than twice the average for similarly sized non-hub metros. American Airlines' CLT hub alone supports nearly 150,000 jobs and $30 billion in annual economic output across North Carolina, part of a total American Airlines economic footprint in the state estimated at roughly $40 billion. The current ten-year Airline Use and Lease Agreement, which supported more than $3 billion in capital improvements including the main terminal expansion, the fourth parallel runway now under construction, concourse renovations, and 19 additional gates, was extended for one year in May while a successor agreement is negotiated.

Case Study

How Connectivity Saved Charlotte's Banking Cluster

The clearest evidence of CLT's strategic value to the regional economy came during the Global Financial Crisis. When Wachovia, then Charlotte's largest private employer, collapsed and was acquired by Wells Fargo in late 2008, the consensus expectation was that San Francisco would gradually pull operations to other major existing employment hubs, hollowing out Charlotte's financial services base. It did not happen. Charlotte came through the crisis with minimal net job losses in financial services, and Wells Fargo today employs more people in the Charlotte region than in any other market.

The reason was straightforward: the region was a great place to do business, had a large experienced financial industry workforce, and the robust air service at Charlotte Douglas made it easy for executives and teams to travel to New York, Boston, Washington, and the bank's other major operating centers without losing a workday. Multiple daily nonstops to every major financial center gave Wells Fargo the confidence to maintain and grow significant operations here.

The same connectivity has played the same role in the years since, in landing Honeywell's global headquarters, Truist, TIAA, Vanguard, and most recently Sumitomo Mitsui, Pacific Life, Maersk, and Scout Motors. CLT is not merely a contributor to Charlotte's headquarters magnetism. It is the key to it. The City of Charlotte announced a one-year extension to the Airline Use and Lease Agreement in May 2026, giving both sides additional time to negotiate the successor deal that will shape the next decade of capital investment at the airport.

Section 3: Commercial Real Estate

Charlotte's office market tells two distinct stories. Metro-wide vacancy has actually been declining, falling from a 2024 peak of 14.7 percent to 13.6 percent in early 2026 with positive net absorption in six of the past seven quarters, and trailing four-quarter leasing volume has reached its strongest level since before the pandemic. The Uptown CBD looks worse on the surface, with vacancy widely reported in the low- to mid-twenties (Cushman & Wakefield puts it at roughly 25 percent, CoStar closer to 23 percent), but that headline is heavily concentrated in older vintage product. A growing share of the legacy bank towers along South College Street, the historic spine of the First Union and Wachovia campus, are repositioning under new ownership and finding tenants again at premium rents. Other large blocks of 1970s-vintage space, particularly along South Tryon Street, are exiting the office market altogether through residential and mixed-use conversion. The 458,000-square-foot former Wake Forest University Charlotte Center on North College Street, vacated when Bank of America's lease expired in 2023, traded last year to a buyer planning multifamily and retail uses. Vanguard's consolidation of five Airport-submarket offices into its newly acquired 700,000-square-foot owner-occupied campus at 2405 Governor Hunt Road in University Research Park has also weighed on the metro number, though that move did not affect the CBD directly. The picture beyond Uptown is materially better. Midtown / South End is running at roughly 11 percent vacancy with 678,000 square feet of twelve-month absorption, the strongest of any submarket, and demand for modern Class A and A+ space remains strong across the metro.

The clearest evidence of that demand sits at 1111 South Tryon, the second tower of Riverside Investment & Development's Queensbridge Collective project at the gateway between Uptown and South End. Originally planned as 356,000 square feet of office above 346 residential units, the developer modified the project in December 2025 to convert two residential floors into office space for Ernst & Young, bringing the office portion to roughly 400,000 square feet above 304 apartments. Anchor tenants now include Moore & Van Allen (206,000 square feet), Pacific Life (68,000), Pamlico Capital, and EY, with the office portion approximately 90 percent preleased ahead of mid-2028 completion. The broader market has caught up to support it: more than thirty leases larger than 30,000 square feet were signed in the year through the first quarter, up from twenty the year before, led by JPMorgan Chase (140,000 square feet at One Piedmont Town Center in SouthPark), American Express (91,000 at Legacy Union), Citigroup (59,000 at the Gragg Building in Ballantyne), and Charles Schwab (30,000 at 110 East in South End). New Class A+ construction of any scale is exceptionally rare nationally in this cycle, and Charlotte is one of only a handful of U.S. metros with a project of Queensbridge's size moving forward.

Demand for existing space is widening to include the best-located older buildings. Sumitomo Mitsui's 194,000-square-foot sublease at 301 South College Street, the former Wells Fargo East Coast headquarters, anchors what had been a nearly empty 994,000-square-foot tower. Scout Motors' 145,000-square-foot lease at the new Commonwealth development in Plaza Midwood marked the first major office commitment in that neighborhood and has prompted developer Crosland Southeast to file plans for a second 150,000-square-foot building on the adjacent parcel. The "flight to quality" is also reaching down into recently renovated mid-vintage properties. Tourmaline's One South, a 1974-built former bank headquarters renovated in 2023, has taken occupancy from roughly 50 percent to 85 percent over four years, lifting asking rents into the high-$40s/SF, and Cousins is now underway on a similar repositioning at 201 North Tryon.

The same pattern is showing up in investment sales. Trailing four-quarter office investment volume reached a three-year high of $1.5 billion in the first quarter, up 44 percent year over year. At the top, institutional and REIT capital has returned to core trophy product: Cousins paid $317.5 million ($497 per square foot) for the 2017-built 300 South Tryon in February, and Highwoods paid $223 million ($540 per square foot) for the 90 percent-leased Legacy Union 6Hundred in November. At the bottom, opportunistic funds are clearing distressed assets at deep discounts. Highland Ventures took 525 North Tryon at $52 per square foot, a 60 percent discount to last trade, and Riverside Investment & Development with partner Singerman paid $36.5 million for the 800,000-square-foot former Two Wells Fargo Center at 301 South Tryon with plans for a complete mixed-use redevelopment beginning in 2027. The former Duke Energy headquarters on South Church Street is becoming the 460-unit Brooklyn & Church apartment project for Q4 2027 delivery, and 400 South Tryon, in foreclosure since 2024, is now headed for housing and hotel conversion. Charlotte Center City Partners estimates roughly $2 billion in announced conversions and renovations on top of $2.4 billion in new construction, enough older inventory leaving the market to support a meaningful tightening even as the headline vacancy number stays elevated in the near term.

The industrial market is going through a similar adjustment on a larger scale and longer cycle. Developers added more than 40 million square feet of industrial space across the metro in the four years through 2025, an unprecedented expansion that pushed availability above 10 percent and gave tenants the upper hand for the first time since 2019. The market is now absorbing that supply rather than chasing it. Twelve-month net absorption reached 4.9 million square feet through the first quarter, deliveries will fall by more than half in 2026, and availabilities in the largest big-box facilities, those above 400,000 square feet, have already tightened by roughly 800 basis points from their mid-2024 peak. Rent growth has moderated to 3.1 percent year over year but continues to outpace the national rate, and the lease pipeline reflects the breadth of demand. Notable leases include Amazon's 450,000 square feet at AXIAL Rapid Commerce in west Charlotte, Walmart's $122 million purchase of the 1.2-million-square-foot Kings Mountain Corporate Center in Gaston County, UTZ Brands in Gaston, Carolina Beverage Group in Iredell, and Jabil Electronics taking the former Gildan Yarns facility in Rowan. Jabil is investing $500 million in Salisbury to upgrade the former sports apparel plant to an advanced manufacturing facility for AI hardware and thermal cooling infrastructure. Institutional capital has returned in force; industrial led every other commercial property type in Charlotte sales volume in 2025, with cap rates on core trophy deals back in the high-4 to low-5 percent range.

Section 4: Population Growth and Geographic Advantages

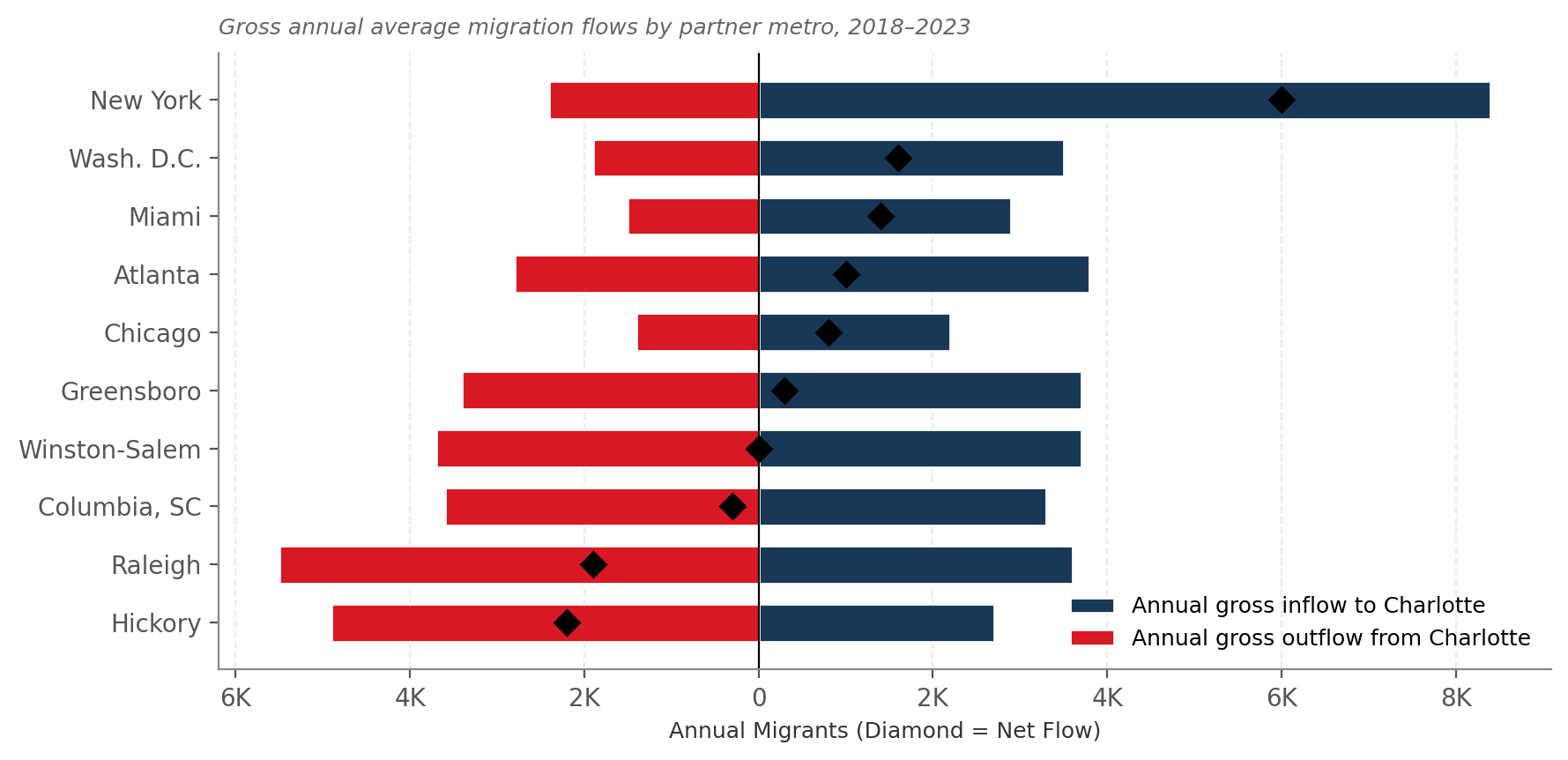

Charlotte continues to lead the nation in raw population gains. The City of Charlotte added the most new residents of any U.S. city in the latest Census estimates (+20,731), while the broader metro is sustaining solid 1.4 percent average annual growth. The metro area led the nation in domestic net migration this past year. Inflows are primarily from the Northeast, Midwest, Florida, and the West Coast, drawn by relatively attainable housing, abundant job opportunities, and quality of life. Net inflows from New York alone average roughly 6,000 residents a year, dwarfing every other source.

The geography of growth tells an important story. The robust growth in the City of Charlotte reflects the City's size and geographic reach, with new areas opening up for development along the I-485 beltway within the city limits. Charlotte is expanding further out as well. The metro's outer-ring counties are now expanding faster than its core, with Lancaster (South Carolina) growing at better than 4 percent annually and York County, anchored by Rock Hill and Fort Mill, now the metro's fastest-growing large county. Scout Motors' EV assembly plant under construction in Blythewood — 75 miles down the I-77 corridor in Richland County — will further strengthen the economic integration between Charlotte's management and talent hub and global connectivity and South Carolina's growing industrial base. The Queen City increasingly functions as a regional hub and command center rather than a single-state economy. The broader CSA includes the neighboring Hickory-Lenoir-Morganton MSA, as well as outlying areas such as Albemarle, Shelby, and Marion, and boasts a population of 3.5 million.

This bi-state geography is increasingly visible in the goods-movement layer of the regional economy as well. South Carolina's competitive tax environment continues to pull distribution capacity across the line: York County alone absorbed nearly 575,000 square feet of net industrial space over the past twelve months, while Gaston County to the west absorbed roughly 1.4 million square feet, the third-largest gain in the metro. Rowan County, anchored by Salisbury, led every Charlotte submarket with more than three million square feet of net absorption, including the 2.1-million-square-foot 85 North Logistics Center and the 730,000-square-foot Overlook 85 facility now in Google's hands. The pattern mirrors what is visible in the migration data: as core counties fill in and prices rise, the activity cascades outward into adjacent counties with more land, lower costs, and direct access to the core. Charlotte's bi-state geography gives it an unusually wide spillover zone, and the goods-movement footprint is broadening at the same pace as the residential one.

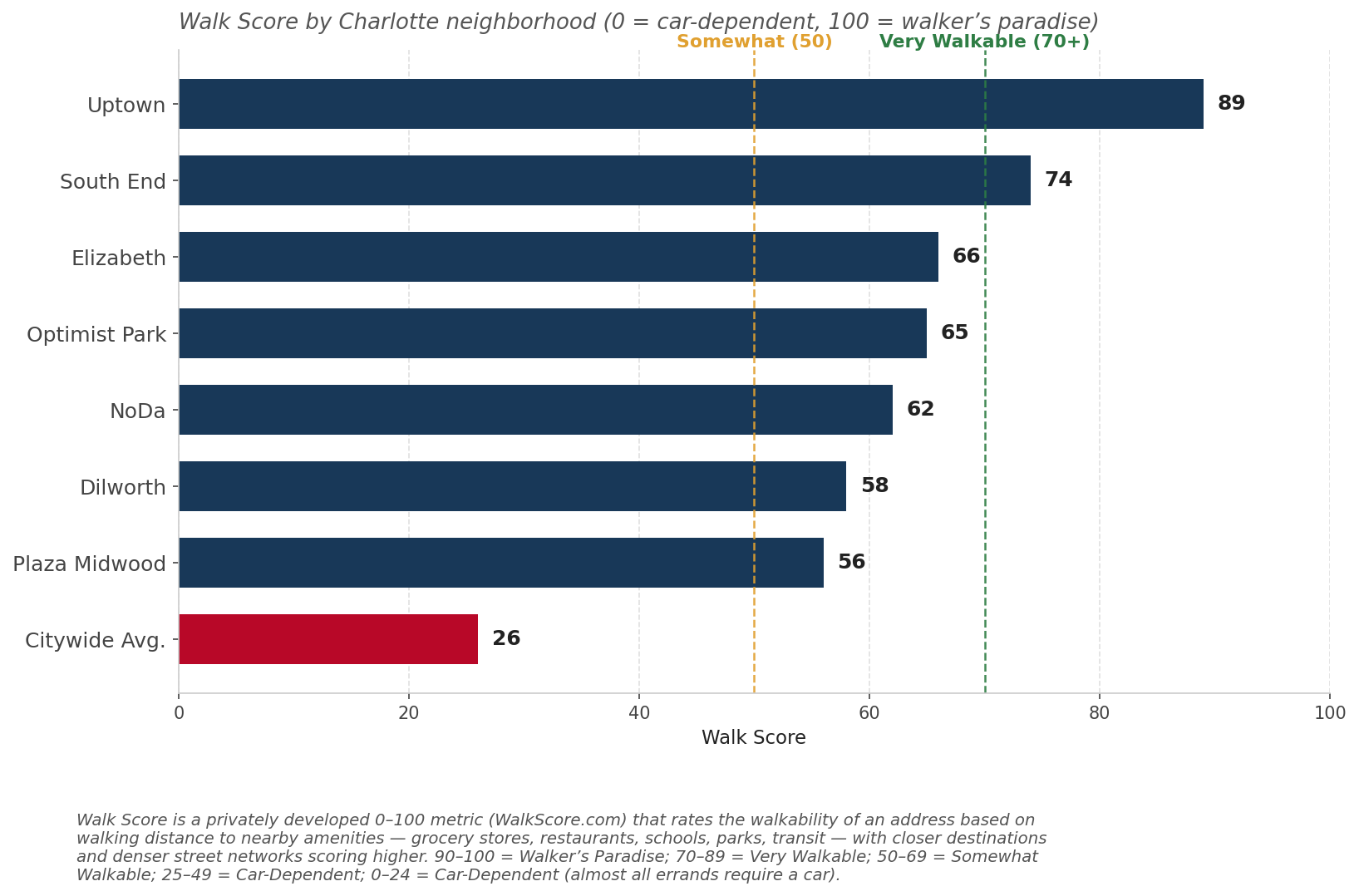

Section 5: Livability, Walkability, and Transit-Oriented Growth

Rapid growth brings challenges, particularly around infrastructure and livability. Citywide, Charlotte still reflects its sprawling nature. ParkScore ranks Charlotte near the bottom among major U.S. cities due to access and equity gaps despite a respectable total acreage and growing network of greenways. The overall Walk Score — a privately developed metric that rates the walkability of a specific address or neighborhood on a 0-to-100 scale based on the proximity of nearby amenities like grocery stores, restaurants, schools, parks, and transit — sits at a car-dependent 26. Yet that aggregate number badly understates what is actually happening on the ground. Vibrant urban pockets are absorbing a disproportionate share of new residential demand, and they look almost nothing like the rest of the city.

South End, which has seen intense apartment development the past 15 years, stands out with a Walk Score of 74, very walkable thanks to the Rail Trail, the light rail, breweries, restaurants, and dense mixed-use development that has reshaped the district over the past decade. Areas all along the light rail line are seeking to emulate South End's success, attracting a large proportion of the younger population that moves to Charlotte each year, many of whom do so without an automobile. The Northern Light Rail Corridor (the LYNX Blue Line from Uptown through Optimist Park, NoDa, and Sugar Creek to UNC Charlotte) exemplifies successful transit-oriented development. Thousands of apartment units are rising or recently completed in Optimist Park, NoDa, and the Sugar Creek/The Pass area. These projects are transforming former industrial land into vibrant mixed-use districts that better connect Uptown jobs to the region's largest university and are also attracting office development in their own right.

Infrastructure Watch

Three Tests of Charlotte's Collaborative Compact

Charlotte's competitive edge has never come from any single asset. It has come from a willingness of business, labor, and government to find common ground and act. The same collaborative approach that built Bank of America and one of the nation's largest banking centers, attracted corporate headquarters like Honeywell, and turned Charlotte Douglas into one of the nation's ten busiest by passenger traffic is being tested on three fronts in 2026, and the outcome will shape the metro's trajectory for the rest of the decade.

I-77 South Express Lanes

The proposed elevated toll lanes between Uptown and the South Carolina state line, estimated at $3.2 billion with NCDOT pursuing a public-private partnership, were effectively shelved this spring. The Charlotte City Council voted 6-5 on May 11 to rescind the city's prior support. The Charlotte Regional Transportation Planning Organization followed on May 20, voting by supermajority to rescind regional support. NCDOT has now confirmed it will withdraw roughly $700 million in committed state funding from the corridor, and regional planners estimate it could be ten years before another credible plan emerges. The equity concerns about elevated lanes through historically Black neighborhoods such as McCrorey Heights and Wesley Heights are real, and the I-77 North toll experience has been politically painful. But the corridor that connects Uptown to CLT and to South Carolina's industrial base now has neither a plan nor a budget, and congestion on one of the metro's most critical economic arteries will continue to worsen.

The Airline Use and Lease Agreement

The current ten-year lease between the City of Charlotte and American Airlines and five other carriers was scheduled to expire June 30, 2026, but the city announced a one-year extension in May to allow more time for negotiations on a successor deal. The next agreement will govern how Charlotte Douglas operates and what construction projects it undertakes over the next decade. The current lease covered roughly $3 billion in capital improvements. Negotiations have been complicated by an organized labor campaign over wages and benefits for subcontracted airport workers represented by SEIU 32BJ. The city has noted the lease cannot legally regulate subcontractor pay, but the underlying workforce concerns are legitimate and need to be addressed through appropriate channels. The risk is that an additional year of delay erodes leverage and pushes off the capital commitments the airport needs to maintain its competitive position.

Brooklyn Village

The transformative seventeen-acre Second Ward redevelopment, meant in part to acknowledge the destruction of a thriving Black neighborhood under urban renewal in the 1960s and '70s, has effectively collapsed as a public-private partnership. The Peebles Corporation lost control of the first-phase parcels in May 2026 when its lender, Atlanta-based Peachtree Group, filed to foreclose on May 5 and acquired the deed for $24.4 million. Peebles still expresses interest in future phases at the county-owned Marshall Park and former Board of Education sites, but Mecklenburg County halted negotiations last August after Peebles missed a July 2025 deadline to demolish the former Board of Education building. A decade after the initial county vote, the largest infill development opportunity in Uptown sits largely idle.

The Counterexample — Transit

Charlotte's collaborative compact has not broken down everywhere. On November 4, 2025, Mecklenburg County voters approved a one-cent sales tax increase by 52.28 percent, generating an estimated $19.4 billion over 30 years for a transformative expansion of the region's transit and transportation network. The tax takes effect July 1, 2026, with 40 percent of revenue directed to rail, 40 percent to roads and pedestrian infrastructure, and 20 percent to bus service. Rail priorities run in sequence: the Red Line commuter rail from Uptown to Huntersville and Davidson, the Silver Line light rail from CLT Airport to Bojangles Coliseum, a six-mile extension of the Gold Line streetcar, and the Blue Line extension to Pineville. The vote is already shaping private capital allocation. The 55-acre Iron District redevelopment on the former Charlotte Pipe & Foundry site, which breaks ground this year between Uptown and South End, sits directly on the planned Silver Line corridor. A new 27-member regional transit authority will oversee the spending.

These tests will not be settled in one year. They are foundational to keeping Charlotte competitive when the economy gets tested again, as it surely will. The collaborative approach that built modern Charlotte, and that produced the transit referendum, now needs to be applied with the same purpose to a serious reset on Brooklyn Village and a credible successor agreement for the airport lease.

Section 6: The Forecast

Charlotte's GDP and employment growth should continue to outpace national averages through 2030. After a cyclical slowdown in 2025 and early 2026, we expect nonfarm payroll growth to re-accelerate as announced capital deployments convert to hiring, with real GDP growth running comfortably above the projected 2.3 percent U.S. pace. Population gains slow only modestly, supporting continued single-family and multifamily construction. The full forecast is summarized in the table on the following page.

The current slowdown also has a cyclical edge to it. Construction payrolls are declining as the backlog of single-family homes and apartments under construction draws down. Banks are trimming payrolls as well, particularly in roles that can be easily automated. Job growth has also been weighed down by tighter immigration enforcement. We expect these headwinds to gradually fade later this year, particularly once uncertainty surrounding the Iran War and related fallout subsides.

Charlotte MSA Forecast at a Glance

| 2024 | 2025 | 2026F | 2027F | 2028–30F | 5-Yr Avg | |

|---|---|---|---|---|---|---|

| Real GDP growth (%) | 3.6 | 3.8 | 3.2 | 3.1 | 2.6 | 2.9 |

| Nonfarm employment growth (%) | 1.5 | 0.9 | 1.1 | 1.2 | 1.3 | 1.2 |

| Nonfarm employment change (000s) | 21 | 13 | 16 | 18 | 19 | 18 |

| Total population (millions) | 2.88 | 2.94 | 2.99 | 3.04 | 3.16 | — |

| Population growth (%) | 2.3 | 2.1 | 1.8 | 1.5 | 1.3 | 1.4 |

| Population change (000s) | 60 | 60 | 52 | 46 | 39 | 43 |

| Unemployment rate (%) | 3.6 | 3.8 | 4.1 | 4.1 | 4.0 | 4.0 |

| Median household income ($) | 85,900 | 88,900 | 91,600 | 94,800 | 105,200* | — |

| Median home price growth (%) | 4.8 | 5.5 | 3.0 | 3.8 | 4.5 | 3.9 |

| Median price of existing home ($) | 425,000 | 435,000 | 448,000 | 465,000 | 530,000* | — |

| Case-Shiller home prices (%) | 5.5 | 3.0 | 1.0 | 2.5 | 4.0 | 3.0 |

| Total housing permits (units) | 25,900 | 24,000 | 22,000 | 23,500 | 27,000 | 25,300 |

| Single-family permits (units) | 18,950 | 17,500 | 16,000 | 17,600 | 19,600 | 18,500 |

| Multifamily permits (units) | 6,950 | 6,500 | 6,000 | 5,900 | 7,400 | 6,800 |

| Consumer spending growth (nominal, %) | 4.0 | 3.9 | 3.3 | 3.5 | 2.8 | 3.0 |

Section 7: Risks to Watch

The primary risk we hear repeatedly from business leaders is housing affordability. Charlotte's Q1 2026 median sale price reached $444,000, up 5.5 percent year-over-year per local MLS data, though the cleaner repeat-sales read from S&P Cotality Case-Shiller shows Charlotte prices up just 0.9 percent over the year through March 2026, with the national index up 0.7 percent. The 10th consecutive month of national real-price declines suggests the housing slowdown has reached the Sun Belt. Our revised baseline projects Charlotte median home price growth of 3.0 percent in 2026 and 3.8 percent in 2027, rising to a 4 to 5 percent range thereafter as inventory tightens and the announced capital and headcount expansions reach the local housing market, broadly tracking Case-Shiller's directional path while sitting a notch higher. That said, Charlotte remains more affordable than nearly every peer Sun Belt metro at a similar stage of expansion. The median home price-to-income ratio sits at 4.8, comfortably below the 5.0 national benchmark and well under Austin (5.6), Tampa (5.5), Nashville (5.2), and Raleigh (5.1).

Additional Risks

- Housing supply and affordability: If new construction in the outer-ring counties and along the LYNX corridors fails to keep pace with continued in-migration, Charlotte's relative affordability advantage could erode by the end of the decade. Median home price growth has now outpaced wage growth for three consecutive years.

- Governance involving infrastructure capacity and stalled major projects: I-77 South, the airport lease, and Brooklyn Village have each been in some form of study, negotiation, or delay for years. Each by itself is recoverable. Together they signal a slowdown in the public-private collaboration that built modern Charlotte. The recent setbacks (NCDOT pulling I-77 funding, the airport lease pushed out a year, and Peebles losing Brooklyn Village phase one through foreclosure) make a credible reset on all three the most consequential infrastructure imperatives the metro faces this year. At a time when several communities (California, New York City, Seattle, Portland) are turning antagonistic toward successful businesses, good governance is a competitive advantage that may be at risk.

- Financial services consolidation: Finance and insurance employment has historically gone through periodic waves of consolidation. Those previous waves actually worked in Charlotte's favor, as the industry consolidated in Charlotte to tap its deep talent base. While the sector remains the metro's largest single employer, the diversified base built across energy, healthcare, logistics, life sciences, mobility, and technology over the past decade provides a meaningful buffer that did not exist in the 1990s or 2000s. The growing tech presence, however, means that if speculative excesses in the AI boom come undone in a similar way to the dotcom boom, Charlotte and some surrounding areas might be more exposed than they were then.

- National policy shocks: Charlotte is well-positioned for a productivity-led cycle, but trade policy, tax policy, and federal infrastructure spending all carry meaningful sensitivity for the metro's headquarters, manufacturing, and logistics base. The Sumitomo Mitsui, Scout Motors, and Maersk announcements would each have looked different under a different policy environment.

The Final Word

Charlotte is well positioned in a productivity-driven expansion. Firms investing in AI, automation, energy, and advanced capabilities will find fertile ground here. The combination of financial depth, headquarters momentum, emerging transit-oriented districts, abundant land and water, and an integrated cross-border economy that reaches deep into South Carolina makes the Queen City one of the South's standout economies, and one of the nation's, heading into the second half of the decade.

The capital-led national cycle plays directly to Charlotte's strengths. The challenges are real, particularly housing affordability and infrastructure capacity. But the city's diversified base, execution capacity, and geographic advantages provide a strong buffer, and an expansion that looks, from this vantage point, more durable than cyclical.

This report is prepared for informational purposes only and does not constitute investment advice. Information is derived from sources believed to be reliable; however, Southeast Economic Advisors LLC makes no representation as to its accuracy or completeness. © 2026 Southeast Economic Advisors LLC. All rights reserved.