Regional Update

Atlanta Mid-Year Economic Outlook

The capital of the Southeast takes the global stage as the World Cup arrives

Download the full report (PDF)

| Outlook | GDP Growth | Employment | Migration | Investment |

|---|---|---|---|---|

| POSITIVE ▲ | +2.5% ’26–’30 | 3.1M jobs (2.8% jobless) | ~90,000 (2026F) | Top-5 data-center hub |

Executive Summary

This month the eyes of the world turn to Atlanta. The 2026 FIFA World Cup opens on June 11, and Mercedes-Benz Stadium, rebranded Atlanta Stadium for the tournament, will host eight matches through a July 15 semifinal, drawing hundreds of thousands of visitors and an estimated $500 million in economic impact. It is a fitting spotlight for a region that has spent decades turning its location and its connectivity into the role of commercial capital of the Southeast.

Metro Atlanta is the sixth-largest metropolitan area in the United States and the largest economy in the Southeast, a diversified base of logistics, corporate headquarters, financial technology, film, health care, and a fast-growing data-center industry. The Atlanta region supports about 3.1 million jobs, and unemployment fell to 2.8 percent in April 2026, near a record low, even as payroll growth has cooled from its torrid post-pandemic pace to roughly flat, in line with the national slowdown.

Our base case calls for Atlanta real GDP growth of about 2.5 percent a year through 2030, modestly above the projected 2.3 percent U.S. pace, with hiring re-accelerating as data-center, corporate, and health-care investment works through the pipeline. The risks are real. The data-center boom threatens to strain the power grid, downtown office values remain under pressure, the restructuring at UPS is weighing on payroll growth, federal cutbacks have hit the Atlanta-based CDC, and traffic and transit limits remain a drag on a fast-spreading region. But Atlanta’s core advantages, its global connectivity, its corporate depth, and a young and growing talent base, are difficult for any other major metro to match.

Key Takeaways

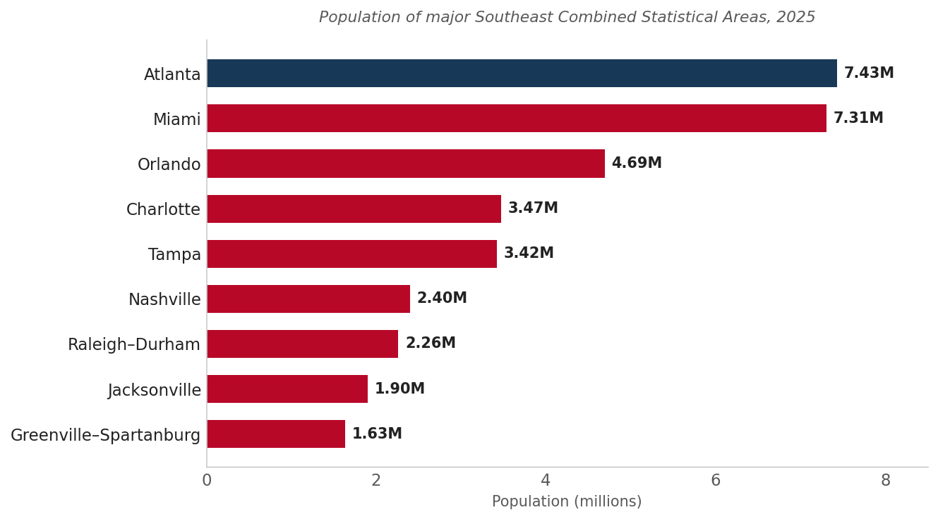

- Atlanta is the economic capital of the Southeast. The Atlanta–Athens-Clarke–Sandy Springs Combined Statistical Area is home to about 7.4 million people, the largest in the Southeast, and the core Atlanta–Sandy Springs–Roswell metro of 6.5 million is the sixth-largest in the nation.

- The labor market is tight but cooling. Metro Atlanta supports roughly 3.1 million jobs, the labor force is at a record high, and unemployment fell to 2.8 percent in April 2026. Payroll growth over the past year has been roughly flat, mirroring the national slowdown after years of rapid gains.

- Connectivity is the foundation. Hartsfield-Jackson, the world’s busiest airport, anchors a logistics network and a corporate base of more than a dozen Fortune 500 headquarters, including The Home Depot, UPS, Delta Air Lines, The Coca-Cola Company, Southern Company, and Intercontinental Exchange. Three interstates converge on the city (I-75, I-85, and I-20), and long before the highway era Atlanta was a rail hub. It remains one today, and is the headquarters of Norfolk Southern.

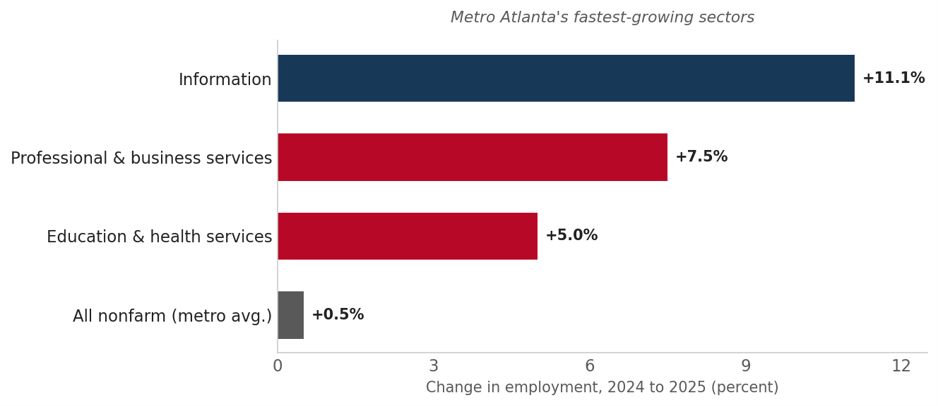

- Growth is rotating toward services and digital infrastructure. Information employment rose about 11 percent from 2024 to 2025, led by a rebound in film and television production rather than data centers, while professional and business services rose about 8 percent and education and health services about 5 percent. Metro Atlanta is also one of the country’s largest data-center markets, though those facilities are capital-intensive and employ relatively few people.

- Housing has cooled to balance. The metro median sits near $390,000 and is roughly flat over the past year, with inventory up sharply and months of supply at the highest level since 2014. Atlanta remains far more affordable than comparable major East Coast metros.

- The watch list is about capacity, not demand. Power-grid strain from data centers, downtown office distress, the UPS restructuring, federal cutbacks at the Atlanta-based CDC, the pending merger of Norfolk Southern into Union Pacific, and chronic traffic and transit limits are the main constraints on an otherwise remarkably diverse and resilient economy.

Section 1: The Capital of the Southeast

No other metro in the Southeast operates at Atlanta’s scale. The core Atlanta–Sandy Springs–Roswell metropolitan area held about 6.5 million people in 2025, the sixth-largest in the country, and the broader Combined Statistical Area, which stretches across some 42 counties from the South Carolina line across into eastern Alabama and takes in Athens, Gainesville, and Rome, is home to roughly 7.4 million. That makes the Atlanta region the largest metropolitan economy in the Southeast and one of the ten largest in the United States, with metropolitan output (MSA basis) of more than $570 billion.

Atlanta’s scale rests on a simple fact of geography turned into an economic asset. Hartsfield-Jackson Atlanta International Airport, the world’s busiest by passenger traffic, puts most of the country within a two-hour flight and the rest of the world within easy reach, and the interstates that converge on the city make it the natural distribution point for the Southeast. A century after Atlanta reinvented itself from a rail junction into an air and logistics hub, that connectivity remains the foundation of the regional economy.

The region is also unusually decentralized. Fewer than one in ten residents live inside the relatively small Atlanta city limits, and employment is spread across Fulton, Gwinnett, Cobb, DeKalb, and a ring of fast-growing suburban counties. The chart below places the Atlanta region among its Southeast peers, where it stands clearly at the top.

Section 2: A Diversified Economy Built on Connectivity

Atlanta has never been a port city, a state capital chosen for its river, or a town that grew up around a harbor or a mine. It exists because of a railroad. In 1836 the Georgia legislature chartered the Western and Atlantic Railroad to run south from Chattanooga, and a survey crew drove a stake to mark where the line would end. The settlement around that stake was called Terminus, the end of the line. It became Marthasville in 1843 and Atlanta in 1847, the name offered as the feminine form of Atlantic in a nod to the railroad. By 1846 two more lines had reached the same point, one running east toward Augusta and one running south toward Macon and the coast at Savannah, and the terminus had become a junction. The junction became a city.

That pattern has repeated at every technological turn since. When the interstate system was built, three of its main arteries met here: I-75, I-85, and I-20, all ringed by the I-285 perimeter. When commercial aviation matured, Atlanta became one of the first true connecting hubs and now runs the busiest passenger airport in the world. And when commerce moved onto fiber, the lines met here again. The carrier hotel at 56 Marietta Street downtown holds the largest concentration of networks in the Southeast, an interconnection point that sits on long-haul fiber running from Florida to New York, where hundreds of carriers exchange traffic. It is the fiber equivalent of an interstate interchange, and the same logic that made Terminus a city now routes the region’s data.

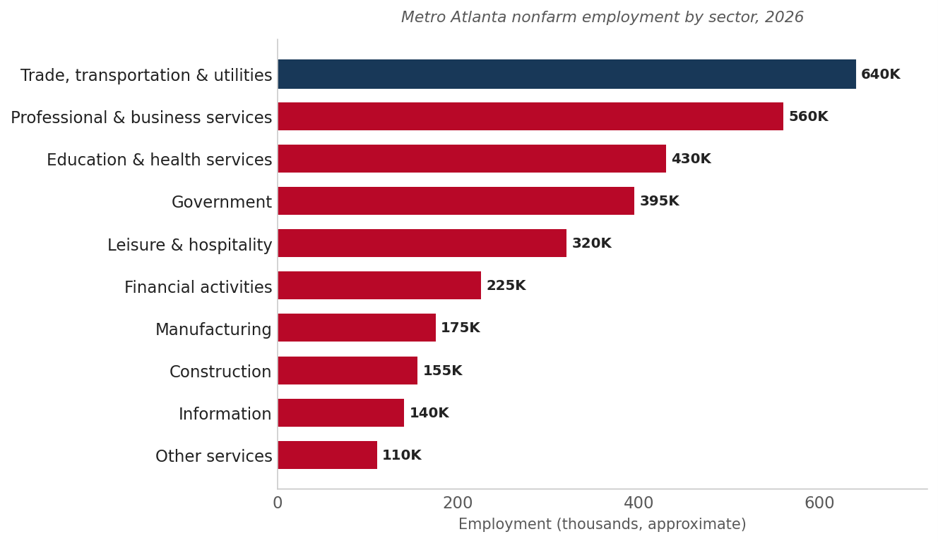

Atlanta’s economy is notable less for any single dominant industry than for how broadly it is spread. Trade, transportation, and utilities, the supersector that captures the region’s vast logistics base, is the largest employer, but it accounts for only about a fifth of metro jobs. Professional and business services, education and health care, government, and leisure and hospitality each anchor large shares of their own, giving the region a balance that few fast-growing Sun Belt metros can claim.

The corporate base runs deep. More than a dozen Fortune 500 companies are headquartered in metro Atlanta, among them The Home Depot, UPS, Delta Air Lines, The Coca-Cola Company, Southern Company, Genuine Parts, and Intercontinental Exchange, the owner of the New York Stock Exchange. Financial technology is a particular specialty. By one widely cited estimate, about 70 percent of all U.S. payment-card transactions are processed through systems based in Georgia, the cluster known as Transaction Alley, anchored by payments firms such as Global Payments and Corpay and by Intercontinental Exchange. In the labor statistics these jobs are counted under financial activities, not information.

Two of Atlanta’s large corporate headquarters tie directly back to the supersector. Delta Air Lines, the dominant carrier at Hartsfield-Jackson, began as a Louisiana crop-dusting operation and took its name from the Mississippi Delta region it first served, before moving its headquarters to Atlanta in 1941. Southern Company, the Atlanta-based parent of Georgia Power, Birmingham-based Alabama Power, and Gulfport-based Mississippi Power, along with Southern Company Gas and the wholesale generator Southern Power, is one of the largest electric utilities in the country and the utility anchor of a metro whose power demand is now climbing on the back of the data-center boom.

Two other engines round out the picture. Georgia’s film and television tax credit has made metro Atlanta one of the largest production centers in the country, supported by studios such as Trilith south of the airport, Assembly in Doraville, and Tyler Perry Studios at the former Fort McPherson site, with a deep crew and contractor base. And health care has been the region’s most reliable job creator, adding tens of thousands of positions in recent years through systems including Emory, Piedmont, Northside, and Wellstar. Atlanta is also home to the Centers for Disease Control and Prevention and the American Cancer Society. Georgia Tech, Emory, Georgia State, and the University of Georgia supply a steady pipeline of graduates across all of it, including top-ranked bioengineering and bioinformatics programs.

The trade in trade, transportation, and utilities is not only freight. Atlanta long ago turned itself into one of the country’s leading marketplaces for wholesale commerce and conventions, a business that runs on the same connectivity. AmericasMart, the downtown wholesale center that opened in 1957 as the Atlanta Merchandise Mart, spans about seven million square feet across three buildings and hosts the Atlanta International Gift and Home Furnishings Market, among the largest wholesale home and gift shows in the world, drawing buyers from every state and dozens of countries. For decades, Atlanta hosted the Bobbin Show, the largest annual trade show for the sewn products and apparel manufacturing industry, before that role passed to the textile and sewn-products expositions the center stages today. The convention economy that grew up around the airport and the highways, anchored by the World Congress Center, the Mart, and one of the largest hotel inventories in the South, is a significant employer in its own right.

For five weeks this summer, Atlanta is a World Cup city. The state-of-the-art Mercedes-Benz Stadium, temporarily renamed Atlanta Stadium under FIFA’s sponsorship rules, will host eight matches between June 15 and a July 15 semifinal, and a free fan festival at Centennial Olympic Park will draw crowds downtown. The region even built a new home for the sport: the Arthur M. Blank U.S. Soccer National Training Center, a $200 million complex in Fayette County, opened this spring. Organizers estimate the tournament will generate more than $500 million in regional economic impact, concentrated in hospitality, retail, and transportation. The event captures what Atlanta has spent decades building. The same assets that made the region a logistics and corporate hub, a world-class stadium, the busiest airport on the planet, and a deep hospitality sector, are what let it host eight World Cup matches without breaking stride. The 1996 Olympics helped debut Atlanta as a global city. Hosting the 2026 World Cup is a reminder that it remains one.

Connectivity also built Atlanta’s cultural reach. The city was the first in the South to land major league professional sports, when the Braves arrived from Milwaukee and the Falcons began play in the same downtown stadium in 1966. The Braves became a regional team because Atlanta’s signal carried. WSB, the South’s first radio station when it signed on in 1922 with call letters its owners read as “Welcome South, Brother,” sent Braves baseball across the region on a clear channel that reached far beyond Georgia. In 1976 Ted Turner bought the team and put its games on his Atlanta station and then onto a satellite, building the Superstation that became TBS and turning a local club into a national one. For a generation of fans from the Carolinas to the Gulf, the Braves were the team you could always find, and Atlanta was the city on the dial.

Section 3: Growth Engines and Headwinds

Two very different growth stories are unfolding at once, and it is easy to confuse them. The first shows up in the jobs data: information employment rose about 11 percent from 2024 to 2025, the fastest of any supersector. That gain is driven mainly by a rebound in film and television production after the recent industry slowdown, the part of the information sector that actually employs large numbers of people, rather than by data centers. Professional and business services and health care were close behind.

The second story is digital infrastructure, and it shows up in capital rather than headcount. Metro Atlanta is one of the largest data-center markets in the country. Amazon Web Services alone has committed at least $11 billion to data centers in Butts and Douglas counties, a project expected to create only about 550 permanent jobs, which captures the pattern: these facilities draw enormous investment but directly employ relatively few people. The build-out is large enough to reshape state policy. Regulators have approved a $16.3 billion Georgia Power plan to expand generation, driven mainly by data-center load, and managing demand without driving up costs for households and other businesses is now one of the central economic-policy questions in the state. A second-order supplier base is forming around it, from transformer and switchgear makers to electrical-component plants.

Investment is broadening well beyond data centers. In early 2026 the Belgian biopharmaceutical company UCB announced a $2 billion biologics manufacturing plant at Rowen, a planned 2,000-acre research community in Gwinnett County positioned between Atlanta and Athens, one of the largest investments in state history and a marquee win for the region’s growing life-sciences cluster. Mercedes-Benz is expanding its North American headquarters and adding an R&D center, and Salesforce, Microsoft, Google, and others continue to add corporate and engineering jobs. The mix of capital-heavy data centers and jobs-rich corporate and life-sciences operations is, increasingly, Atlanta’s edge.

The recruitment pipeline behind those headlines has stayed full. Georgia booked its strongest year on record for business recruitment in fiscal 2025, with state officials citing more than $26 billion in committed investment and roughly 23,000 new jobs across some 423 expansions and relocations, and metro Atlanta captured a large share of the corporate operations within that total. The clearest recent signal came in March 2026, when Yamaha Motor said it would shift its U.S. headquarters from California to Kennesaw over the next two years, deepening a Georgia presence that already exceeds 2,300 workers. Shared-services and back-office wins from CRH, AIG, and TriNet have added white-collar jobs across the northern suburbs, and downtown is drawing fresh private capital, from the $5 billion Centennial Yards build-out to the South Downtown restoration and the proposed Forge Atlanta tower. The reasons companies give rarely change: workforce, connectivity, and cost.

The expansion has not been without disappointments. UPS, long an anchor of Atlanta’s logistics economy, announced the largest restructuring in its history in 2025, cutting tens of thousands of positions nationwide as it reduced Amazon delivery volume, with additional Atlanta-area facility closures planned for 2026. Downtown office values remain under pressure after decades of decentralization, even as investors bet on a revival around Centennial Yards and Georgia State University. And Rivian’s large electric-vehicle plant near Social Circle, paused in 2024, resumed in 2025 with a federal loan and is now also home to the company’s East Coast headquarters in Atlanta. The sharpest recent blow has been federal. As the home of the CDC, Atlanta has been hit hard by Washington’s retrenchment: the agency shed roughly a quarter of its workforce in 2025 through layoffs and early retirements, proposed budgets would cut deeper, and other federal grants and offices in the region have been trimmed as well. Each is a reminder that even a diversified economy carries cyclical, company-specific, and now policy risk.

Section 4: Talent, Migration, and Housing

Population growth is still one of Atlanta’s most dependable economic inputs, but its composition is shifting. The broader Combined Statistical Area added about 73,000 people in the year to mid-2025, and the core Atlanta–Sandy Springs–Roswell MSA accounted for roughly 62,000 of that, the third-largest one-year numeric gain of any U.S. metro, behind only Houston and Dallas. The mix behind those numbers is what stands out. Net domestic migration into the core has flattened and turned slightly negative, while natural increase and, above all, international migration now account for essentially all of the gain. That swing factor leaves the region more exposed to shifts in federal immigration policy than it was a decade ago. A young, diverse, and well-educated workforce, fed by more than 60 colleges and universities, remains the single most common reason companies give for choosing the region.

Growth is also spreading outward, which is why the broader Combined Statistical Area is now gaining faster than the core metro. As prices and congestion build toward the center, households and employers are pushing into the outer ring, and the core counties of Fulton, DeKalb, and Clayton grew only about 1 percent. Hall County, home to Gainesville and a new $134 million inland port on the Norfolk Southern line to Savannah, and Jackson County, on the Interstate 85 corridor toward Athens and anchored by SK Battery’s electric-vehicle plant in neighboring Commerce (Banks County), were among the fastest-growing counties in the state. This is the practical case for reading the region as a CSA: its labor and housing markets now stretch from the airport out to Athens and Gainesville.

Housing has shifted from frenzy to balance. After double-digit price gains in 2021 and 2022, the metro median has settled near $390,000 and is roughly flat over the past year, with active listings up sharply, months of supply at the highest level since 2014, and homes taking about two months to sell. New apartment construction, which peaked in 2024 and 2025, is now tapering. For all the talk of rising costs, Atlanta remains 30 to 40 percent cheaper than comparable coastal metros, and that relative affordability is still a powerful draw.

The constraint is increasingly about getting around rather than getting in. Metro Atlanta is famously spread out and car-dependent, traffic congestion is a persistent drag on productivity and quality of life, and the rail transit network reaches only a fraction of the region. Continued growth will depend on housing supply keeping pace and on steady, if incremental, progress on mobility.

Section 5: Commercial Real Estate

Atlanta’s property markets mirror its economy: large, diversified, and adjusting to a higher cost of capital, with performance split increasingly by quality and location.

Office

The office market is working through the same reset as the rest of the country, but from a position of relative affordability. Vacancy sits near 16.5 percent across the roughly 330 million square foot market, close to a cyclical high but edging down over the past year as leasing stabilizes. Asking rents average about $30 per square foot, well below the $37 national average, and new construction has slowed to a trickle, barely one million square feet, or 0.3 percent of inventory, with about two-thirds of it preleased. That discipline should keep the market from a deeper oversupply problem.

Beneath the average is a sharp split by quality. Top-tier towers ask about $38 per square foot but carry vacancy near 24 percent after a wave of new trophy supply, while older commodity space is barely 6 percent vacant. Tenants are trading up, as the best buildings gained occupancy over the past year even as lower-tier product gave it back. The pattern is clearest in the priciest in-town submarkets, Midtown, West Midtown, the Eastside Beltline, and Buckhead, which post both the highest rents and the highest vacancies as new and repositioned space competes for the same knowledge-economy tenants.

Demand still has real anchors. Norfolk Southern, despite its pending merger with Union Pacific, renewed its roughly 750,000 square foot Midtown headquarters complex for five more years in April 2026, and Cargill, Google, and others keep expanding in Tech Square. Capital markets remain the soft spot. Sales volume ran about $1.7 billion over the past year, well below the $2.7 billion five-year norm, values have reset toward $196 per square foot, and cap rates have climbed toward 7.5 percent, higher for Class A. Several large, half-empty towers traded at deep discounts this spring, including One and Two Midtown Plaza at 37 to 42 percent vacancy, even as medical and trophy assets still command premiums. Expect more adaptive reuse and office-to-residential conversion as owners reposition obsolete space.

Retail

Retail is the quiet strength of Atlanta’s property markets. Vacancy sits near 4.3 percent, among the tightest of any major property type and the product of years of almost no new construction set against steady population and income growth. Asking rents run close to $24 per square foot and have risen about 3.6 percent over the past year, faster than the national pace, as scarce space and quick leasing keep the leverage with landlords. Development remains minimal, barely 0.2 percent of inventory under way and most of it preleased or built to suit for national operators such as Chick-fil-A, Starbucks, and Circle K, alongside the occasional grocery-anchored center. With little speculative supply in the pipeline, the gap between demand and available space should persist.

The strength is broad but tilts to the high-growth suburbs. The northern counties, where households and incomes are expanding fastest, have taken an outsized share of leasing, while in-town districts draw on rising residential density and a wave of mixed-use development, from the fully leased High Street project in Dunwoody to the new storefronts taking shape around Centennial Yards and South Downtown. Investment has held firm even as deal flow thinned, with sales volume of roughly $364 million over the past year, pricing near $225 per square foot, and cap rates around 7.2 percent. For a metro adding tens of thousands of residents a year, a supply-constrained retail market is less a cyclical story than a structural one.

Industrial

Atlanta runs one of the largest industrial markets in the country, and it got there the way the city did, by sitting where the lines cross. The metro’s warehouse and distribution base is built on the convergence of I-75, I-85, and I-20, the Norfolk Southern and CSX rail networks, and a deepwater outlet at the Port of Savannah that has become one of the fastest-growing container gateways in the nation. Cargo landed in Savannah reaches Atlanta in about four hours by truck up I-16 and I-75, or overnight by double-stack train, which is why the region functions as the inland distribution hub for the Southeast.

The investment picture, drawn from CoStar, shows a market that has repriced higher and stayed active. Trailing twelve-month sales volume measures about $6.5 billion across roughly 1,100 transactions, above the prior five-year averages of $4.9 billion and 1,000 deals. Market pricing now sits near $128 per square foot, up close to 10 percent over the year and well above the $114 three-year average, with the market cap rate around 6.5 percent. Logistics product prices near $123 a foot, specialized and manufacturing space near $136, and flex near $172. The soft spot is occupancy. Vacancy has risen to about 8.5 percent, above its longer-run norm, as a heavy pipeline of new big-box deliveries works through lease-up. That is a digestion problem rather than a demand problem, and it is concentrated in the largest-format buildings.

Capital is selective and national. Institutions made up the largest share of buying over the past year at about 38 percent of volume, ahead of private buyers at 35 percent, with users, private equity, and public REITs filling out the rest, and national capital accounted for roughly 77 percent of purchases. The names point to rotation rather than retreat: Blackstone and Franklin Templeton were the largest net sellers as they trimmed and recycled large portfolios, while KKR, GI Partners, TIAA, Apollo, Brookfield, Hillwood, and EQT were among the most active buyers. The deal sheet also captures the demand drivers directly. Amazon bought the Chattahoochee Logistics Center outright as an owner-user, a federal agency acquired a million-square-foot building at PNK Park Loggins, Georgia Power purchased a large facility in Butts County, and two downtown and airport assets traded as data centers, evidence that the same power and fiber advantages behind the region’s connectivity are now pulling capital into industrial real estate.

Geographically, the volume follows the freight. The Airport and North Clayton submarket was the single largest by sales at close to $1 billion, with the I-20 West corridor toward Douglasville and the South Clayton and Henry County corridor around McDonough close behind. These are the big-box, port-facing submarkets that move containers off Savannah. North Fulton and Forsyth command the highest pricing in the market, above $200 a foot, but on smaller infill and flex product rather than bulk distribution.

The forward case rests on the same infrastructure that built the market. Savannah handled close to 5.7 million container units in 2025, its second-busiest year on record, and the Georgia Ports Authority is in the middle of a $4.5 billion expansion that will lift capacity sharply over the next decade. New inland rail terminals, including the Blue Ridge Connector opening near Gainesville this year, will pull more of that cargo directly into the metro’s northern counties. As long as the port keeps growing and the interstates keep meeting here, the demand under Atlanta’s industrial market is structural rather than cyclical. The near-term task is absorbing the space already built. The longer-term trajectory still points up.

Section 6: The Forecast

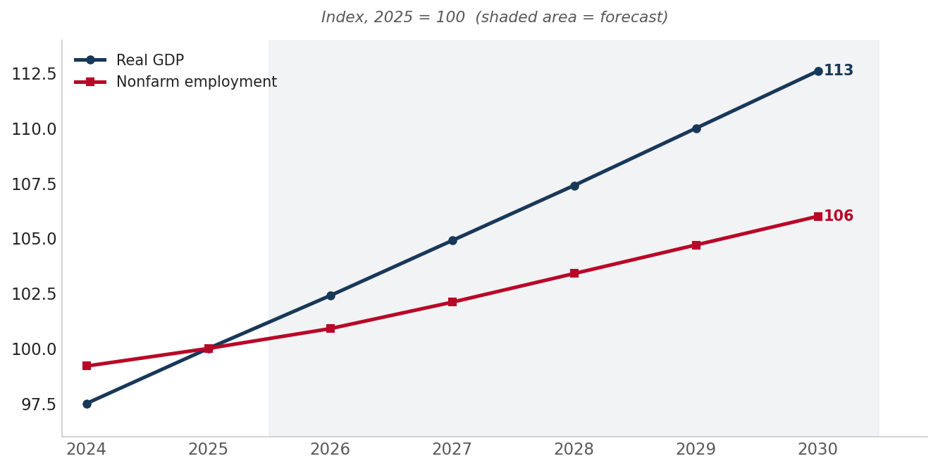

Atlanta’s economy should continue to grow modestly faster than the nation through 2030. We expect payroll growth to re-accelerate from its recent lull as data-center, corporate, and health-care investment converts to hiring, with real GDP growth running a few tenths above the projected 2.3 percent U.S. pace. Population gains stay strong, supporting steady homebuilding, while home-price growth resumes at a healthier, more sustainable pace after the current reset.

| 2024 | 2025 | 2026F | 2027F | 2028–30F | 5-Yr Avg | |

|---|---|---|---|---|---|---|

| Real GDP growth (%) | 4.7 | 2.7 | 3.4 | 3.5 | 3.8 | 3.6 |

| Nonfarm employment growth (%) | 3.4 | 0.3 | 1.2 | 1.2 | 1.3 | 1.3 |

| Nonfarm employment change (000s) | 107 | 9 | 40 | 42 | 42 | 44 |

| Total population (millions) | 7.35 | 7.43 | 7.52 | 7.61 | 7.86 | n/a |

| Population growth (%) | 1.4 | 1.0 | 0.9 | 0.8 | 1.1 | 1.0 |

| Population change (000s) | 103.4 | 72.9 | 66.8 | 63.7 | 80.8 | 74.6 |

| Unemployment rate (%) | 3.4 | 3.1 | 3.4 | 3.6 | 3.6 | 3.4 |

| Median household income ($) | 85,000 | 88,000 | 91,000 | 94,500 | 104,000* | n/a |

| Median home price growth (%) | 4.0 | 1.0 | 2.0 | 3.5 | 4.0 | 2.9 |

| Median price of existing home ($) | 385,000 | 390,000 | 398,000 | 412,000 | 465,000* | n/a |

| Total housing permits (units) | 56,000 | 52,000 | 50,000 | 54,000 | 58,000 | 54,000 |

| Single-family permits (units) | 38,000 | 36,000 | 35,000 | 38,000 | 41,000 | 37,600 |

| Multifamily permits (units) | 18,000 | 16,000 | 15,000 | 16,000 | 17,000 | 16,400 |

Sources: BLS Quarterly Census of Employment and Wages, BEA, U.S. Census Bureau, FHFA, National Association of Realtors; Southeast Economic Advisors estimates. Geography: population, real GDP, and employment are for the Atlanta–Athens-Clarke–Sandy Springs CSA, with employment drawn from QCEW data and GDP growth estimated from it; unemployment, household income, home prices, and permits are for the Atlanta–Sandy Springs–Roswell MSA. *2028–30F values for median household income and median home price are 2030 endpoints, not period averages. F = forecast.

Risks to Watch

- Power and infrastructure capacity. The data-center boom is driving electricity demand far faster than utilities planned for. New generation, transmission, and the question of who bears the cost are now central risks, and capacity constraints could slow the very industry fueling growth.

- Commercial real estate and the logistics transition. Downtown office values remain depressed, and the UPS restructuring is reshaping a workforce that has long anchored the region. Both are manageable but concentrated sources of strain.

- Federal retrenchment. As the home of the CDC, Atlanta is unusually exposed to cuts in the federal workforce and grants. The agency lost roughly a quarter of its staff in 2025, and proposed budgets would cut deeper, with ripple effects across the region’s public-health, research, and contracting ecosystem.

- Housing affordability, traffic, and transit. Prices have outrun incomes in inner neighborhoods, and the region’s car dependence and limited transit footprint remain a structural drag if growth continues to outpace infrastructure.

- Concentration and external shocks. Exposure to air-travel and logistics cycles through Delta and UPS, the policy risk around Georgia’s film tax credit, growing reliance on international migration, and sensitivity to national interest-rate and trade conditions all bear watching.

The Final Word

Atlanta enters the second half of the decade doing what it has done for generations: turning its location into leverage. The airport and the highways made it the hub of the Southeast, the corporate base gave it depth, and a young, growing population keeps refilling the talent pool. The economy is broad enough that no single setback, whether at UPS, at the CDC, in the office market, or on the power grid, threatens the whole.

There are real constraints ahead, and most of them are about capacity rather than demand: power, roads, transit, and housing supply. But the region’s underlying strengths are rare and hard to duplicate. As the world arrives in Atlanta this summer for the World Cup, it will find a city that has become one of the country’s most important economies, and the unquestioned capital of the Southeast.

Download the full report (PDF)

Certification and Important Disclosures

Mark Vitner, Chief Economist at Southeast Economic Advisors LLC, certifies that the views expressed in this report accurately reflect his professional assessment of the subject matter and that no part of his compensation was, is, or will be directly or indirectly related to the specific views expressed herein.

This report is prepared for informational purposes only and does not constitute investment advice. Information is derived from sources believed to be reliable; however, Southeast Economic Advisors LLC makes no representation as to its accuracy or completeness. © 2026 Southeast Economic Advisors LLC. All rights reserved.