Made in the Sunbelt: A Long-Overdue Update

When I wrote Made in the Sunbelt back in July 1993, the global order was undergoing a tectonic shift. Less than four years after the fall of the Berlin Wall, the anticipated “peace dividend” promised a redirection of federal resources toward domestic renewal. At the time, the Southeast was emerging from the early-1990s recession, which eliminated more than 1.7 million factory jobs nationwide and hundreds of thousands across the South.

Yet resilience was already visible along key corridors—most notably Interstate 85 through the Piedmont Crescent, stretching from Montgomery, Alabama, up to Atlanta, Greenville, Charlotte, and up through the Piedmont Triad and Durham up to Richmond, Virginia. Employment rebounded in these areas, supported by early infrastructure investment and a willingness to adapt to a changing economic landscape.

Key Takeaways

- The Southeast is undergoing a structural shift more consequential than anything seen since the early 1990s.

- The region now accounts for roughly 38% of the nation’s population and has captured approximately 55% of national homebuilding activity since the pandemic.

- Since 2020, it has been the only U.S. region with sustained positive net domestic migration and the leading destination for corporate relocations, new manufacturing facilities, and foreign direct investment.

- The South generates roughly 35% of U.S. gross domestic product but has accounted for nearly 45% of national economic growth since the pandemic.

- The South’s Third Industrial Revolution reflects a convergence of electrification, aerospace, AI infrastructure, life sciences, advanced materials, modern logistics, and a robust defense sector.

Our earlier report predated NAFTA and the next major phase of globalization. The decision to grant China Permanent Normal Trade Relations (PNTR) in 2000 accelerated deindustrialization across the Midwest and Northeast, while also eroding the South’s textile, apparel, and furniture industries. Many towns suffered irreversible decline as mills closed and communities hollowed out.

The Southeast did not escape globalization but adapted to it earlier and more effectively than other regions.

The Southeast pivoted earlier than most. South Carolina secured BMW’s Spartanburg plant in 1994, catalyzing the transition from textiles to advanced manufacturing. Tennessee and Alabama built integrated automotive ecosystems combining assembly, R&D, and logistics. The Research Triangle and Austin emerged as national centers for technology and life sciences. Charlotte evolved into a major financial center and the nation’s second-largest banking hub, anchoring major operations for Bank of America, Truist, Wells Fargo, Ally Financial, U.S. Bancorp, and Regions Bank. These moves laid the groundwork for diversified growth, turning vulnerability into competitive advantage.

The Third Industrial Revolution Takes Shape

Three decades later, the Southeast’s transformation is broader, deeper, and more durable and is driven by capability rather than low costs. Engineering talent, university-anchored research ecosystems, integrated supply chains, global connectivity, and reliable power and logistics now define the region’s edge.

Corporate headquarters continue to gravitate toward Dallas, South Florida, Atlanta, Charlotte, and Nashville, drawn by deep labor pools, sustained in-migration of skilled workers, and quality-of-life advantages such as relative housing affordability and cultural amenities. Connectivity—through airports, interstate highways, ports, and digital infrastructure—reduces downtime and enhances predictability in an era of supply-chain volatility.

This is the South’s Third Industrial Revolution: capability-driven, power-constrained, and infrastructure-led.

We describe this era as the South’s Third Industrial Revolution: the first large-scale fusion of manufacturing, energy systems, life sciences, technology, logistics, and defense into an integrated innovation ecosystem. Unlike earlier waves, this convergence creates reinforcing synergies. AI-enabled logistics optimize life-sciences supply chains; aerospace materials deepen automotive and defense manufacturing; and power-intensive infrastructure underpins the AI buildout itself. The result is a resilient economic model capable of withstanding shocks ranging from pandemics to trade disruptions.

Where the Southeast Stands in 2026

For analytical clarity, we define the South as the most economically and culturally cohesive version of the Southeast. While it is tempting to define the region by college football allegiances or NASCAR popularity, the boundary is more deliberate. It includes all states competing in the Southeastern Conference—including Texas, Oklahoma, and Missouri—but excludes Washington, D.C., Maryland, and Delaware, which align more closely with the Mid-Atlantic, as well as West Virginia, which remains more closely tied to the Midwest.

Only the South has sustained positive net domestic migration since 2020, capturing the majority of U.S. population growth.

The 14-state region is now home to roughly 133 million residents, or about 38% of the U.S. population. The Southern economy exceeds $10 trillion in output, accounting for approximately 35% of national GDP. More importantly, since the pandemic recession, Southern states have generated about 45% of U.S. real GDP growth—an outperformance driven by private-sector dynamism rather than temporary fiscal stimulus.

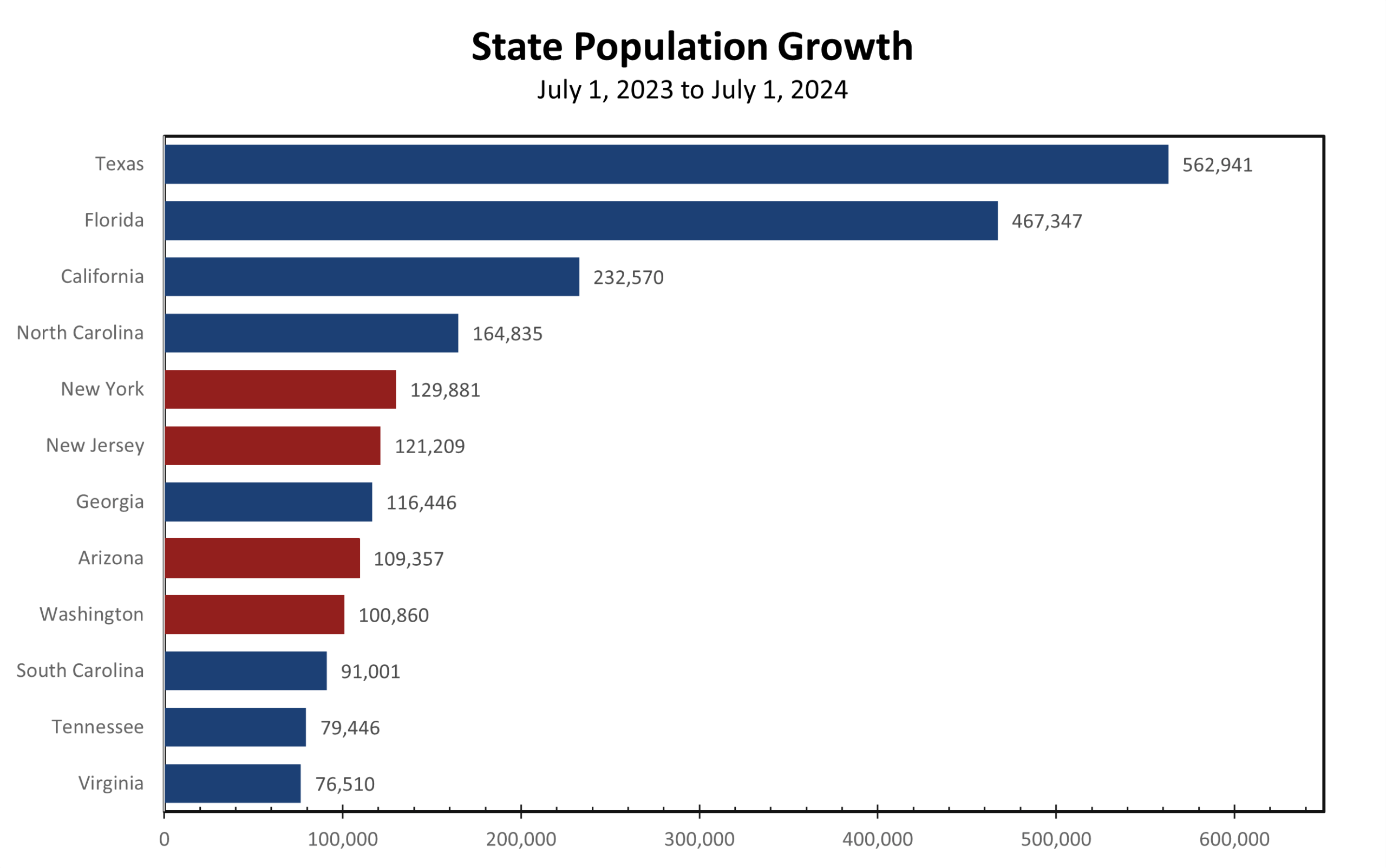

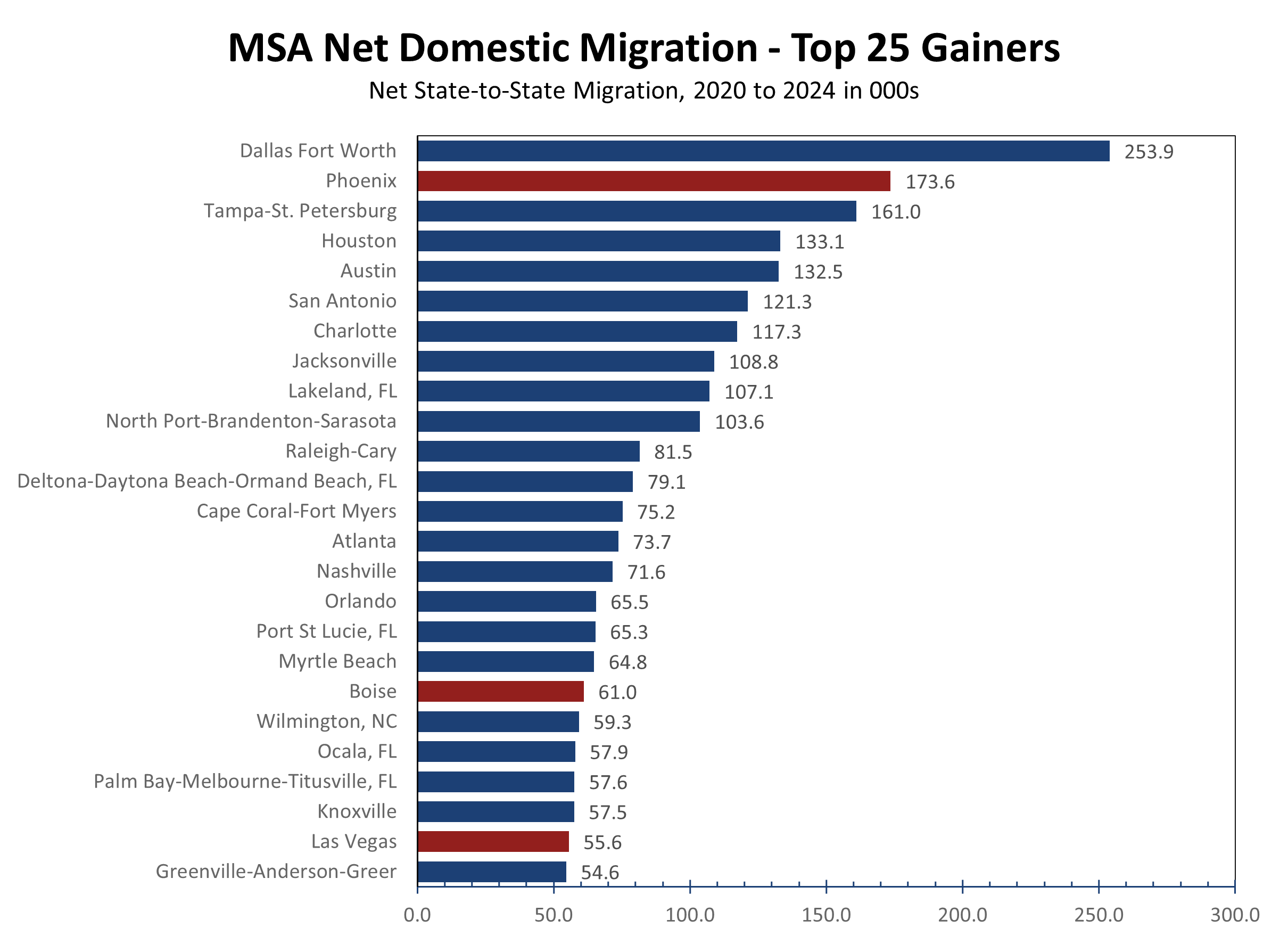

Migration, capital investment, and business expansion have been the heavy lifters. The region added more than 5 million residents from 2020 to 2025, capturing over 70% of total U.S. population growth. Sustained net domestic migration—totaling around 3 million inflows—sets the South apart as the only region with consistent gains, while the Northeast and Midwest experienced outflows. Six of the nation’s top 10 states for population growth in 2024 (Florida, Texas, North Carolina, South Carolina, Georgia, Tennessee) are in the South, as well as 23 of the nation’s top 25 metropolitan areas for net state-to-state migration from 2020 to 2024.

Newcomers to the region are drawn by a powerful combination of abundant job opportunities in high-growth sectors, lower taxes compared to many coastal and northeastern states, and appealing lifestyle amenities such as warm climates, affordable housing, outdoor recreation, and vibrant cultural scenes. The region is also a magnet for retirees, with Florida, South Carolina, Tennessee, and Gulf Coast communities like those in Alabama and Mississippi drawing millions for warm climates, coastal access, and retiree-friendly policies. This demographic influx supports consumer-driven sectors like healthcare, financial services, retail trade, and residential and commercial real estate, further amplifying growth.

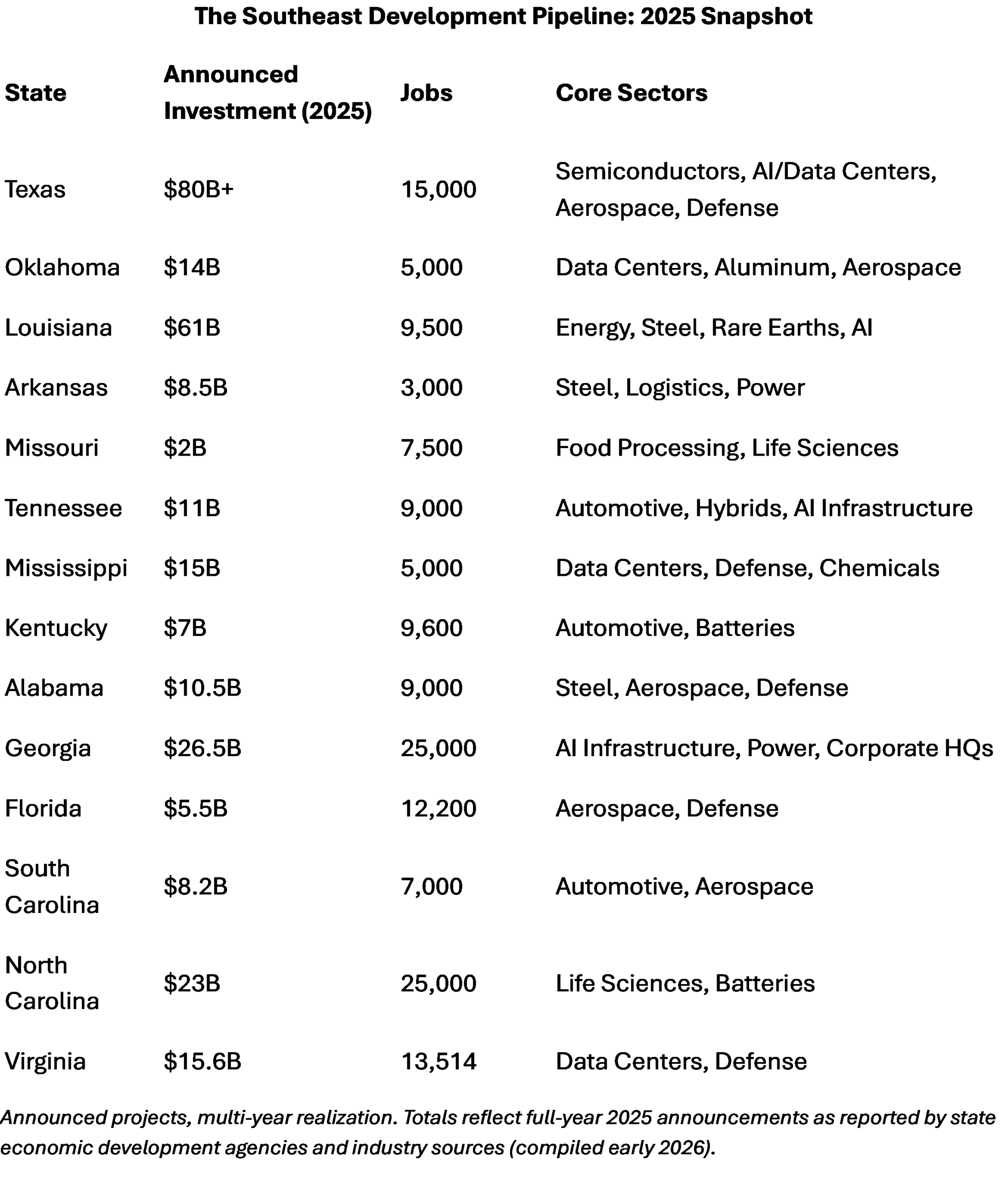

Structural Growth Engines and the Development Pipeline

The South’s enduring advantages—affordable and reliable power, business-ready sites along major transportation corridors, deep labor pools, and collaborative public-private partnerships—have long supported greenfield investment. What has changed is the nature of demand.

This cycle is increasingly capital-intensive and power-heavy, making job growth a less effective yardstick for progress.

Economic development is now driven by converging structural forces: electrification and advanced manufacturing; AI and data-center infrastructure; life-sciences reshoring; port-anchored logistics networks; and an expanding defense sector. Together, these forces have shifted the pipeline from cyclical booms toward sustained, long-duration expansion

Electrification 4.0 and the AI Utility Era

The transition to Electrification 4.0—spanning EVs, hybrids, advanced manufacturing, and AI—has elevated high-capacity electricity to the Southeast’s most critical economic input. Power availability and grid resilience now rank alongside labor and land as binding constraints on growth.

Electricity demand is massive and non-negotiable. Hyperscale data centers and advanced manufacturing facilities routinely consume power measured in gigawatts and operate with zero tolerance for outages. The Southeast’s regulated utility structure, diversified generation mix, and sustained investment in transmission and distribution uniquely position the region to deliver power at scale and on schedule.

In this framework, AI is best understood not as software, but as infrastructure—where electricity is the primary feedstock. Regions that can supply it quickly are capturing the next wave of capital formation.

AI is no longer a software story but rather an infrastructure story, with electricity as the primary feedstock.

That advantage may deepen further if early-stage plans to revive construction at South Carolina’s V.C. Summer nuclear site advance. Under a non-binding memorandum of understanding approved in December 2025, Brookfield Asset Management would complete the two partially built AP1000 reactors abandoned in 2017. If the project reaches a final investment decision targeted for late 2027, it could add more than 2,000 megawatts of carbon-free baseload capacity while relieving balance-sheet pressure on the state-owned utility without incremental customer costs.

While the EV segment has encountered cyclical headwinds, the broader electrification and AI-infrastructure buildout remains intact. Corporate pivots—such as Ford’s recalibration at BlueOval City or Envision AESC’s pause in South Carolina—reflect market adjustment rather than retreat.

Capital continues to flow aggressively into power-intensive platforms, including BMW’s electrification of Spartanburg, Toyota’s battery operations in North Carolina, ArcelorMittal’s electrical steel investment in Alabama, and a growing constellation of hyperscale AI campuses across the region.

Taken together, surging AI-driven power demand, grid investment, and the potential revival of nuclear baseload reinforce the Southeast’s leadership in what can best be described as the AI utility era. This is not a pause in electrification, but a maturation of it.

2025: A Tumultuous Year for Economic Development

The year 2025 proved unusually volatile for U.S. economic development, shaped in large part by policy decisions during President Trump’s second administration. The imposition of broad tariffs on non-North American imports by midyear triggered sharp swings in trade flows, stalled numerous investment projects, and disrupted supply chains across multiple industries. According to S&P Global Mobility, these measures significantly raised costs, with companies such as Ford reporting tariff impacts of up to $3 billion in 2025 alone.

At the same time, a deliberate policy pivot away from electric vehicles (EVs) and certain green-energy initiatives—including reductions in federal incentives and expanded Section 301 tariffs on EV components—contributed to a marked slowdown in new project announcements, particularly in renewable energy. The International Energy Agency noted that this policy uncertainty clouded the global EV outlook, dampening consumer demand amid rising vehicle costs.

Policy uncertainty, not labor costs, was the binding constraint on investment decisions in early 2025.

From April through July, economic development activity languished nationwide, including across the Southeast, as firms delayed decisions while awaiting clarity on trade negotiations and tariff exemptions. Momentum began to recover by August as tariffs were scaled back selectively and new trade agreements emerged. These developments reignited commitments to reshore critical industries, though often with longer timelines and more cautious capital deployment.

Investment rebounded most strongly in capital-intensive, labor-light sectors—data centers, energy and power infrastructure, life sciences, and aerospace—propelling the Southeast to the forefront of the recovery. Many states closed the year with record announced investment totals, even as job commitments moderated due to the increasingly automated nature of these projects.

2025 became a year of record billion-dollar projects but not record job creation.

In that sense, while tariffs and policy shifts caused near-term disruption, they also accelerated domestic manufacturing, infrastructure investment, and innovation—laying the groundwork for longer-term resilience.

Life Sciences and Biomanufacturing: Reshoring in Plain Sight

Life sciences represent one of the Southeast’s most underappreciated reshoring successes. The pandemic exposed vulnerabilities in global pharmaceutical and medical supply chains, accelerating domestic investment in biomanufacturing, medical devices, and therapeutics. North Carolina alone has added more than 13,000 life sciences jobs since 2018, with total employment exceeding 100,000 by 2023. The state now ranks seventh nationally and continues to grow faster than most peers.

Life sciences reshoring may be quieter than semiconductors, but it is far more durable.

Across the Carolinas, Virginia, Georgia, Tennessee, Alabama, and Florida, the region has emerged as a leader in capital-intensive pharmaceutical production, including cell and gene therapies, sterile injectables, active pharmaceutical ingredients, and advanced medical devices. These states benefit from regulatory predictability, cold-chain logistics, deep university partnerships, and a skilled workforce built over decades.

Eastern North Carolina, part of the BioPharma Crescent, has become a biomanufacturing powerhouse. Facilities operated by Thermo Fisher in Greenville, Johnson & Johnson in Wilson, and Pfizer in Rocky Mount anchor large-scale production of sterile injectables and biologics. In the greater Raleigh area, Novo Nordisk’s $4.1 billion expansion in Clayton is adding 1,000 jobs focused on diabetes and obesity treatments, reinforcing the Research Triangle’s global standing. Farther south in Wake County, Holly Springs has emerged as a biomanufacturing epicenter, with major investments from Genentech, Amgen, and Ypsomed supporting hundreds of high-wage jobs and fueling sustained population growth.

That momentum is now extending deeper into the Southeast. In 2025, Eli Lilly announced plans to develop a new large-scale pharmaceutical manufacturing campus in Huntsville, Alabama, marking one of the most significant life sciences investments in the state’s history. The project underscores how biomanufacturing is converging with the region’s strengths in engineering, advanced manufacturing, and defense-adjacent talent, while broadening the geography of pharmaceutical reshoring beyond traditional coastal hubs.

Biomanufacturing clusters tend to expand in place, creating compounding economic returns rather than one-off wins. Facilities scale over time, supplier networks deepen, and research partnerships mature. Reshoring in life sciences is not cyclical. It is structural. Firms are bringing back the foundational building blocks of pharmaceuticals and medical products to improve supply-chain security, enhance resilience, and ensure long-term domestic capacity

Aerospace and Defense: A High-Wage Regional Spine

Aerospace and defense have emerged as a high-wage sector gaining traction across the Southeast. The industry has long maintained a significant presence in the region. Texas has been home to multiple producers of military aircraft, while Lockheed Martin has built C-130 transport aircraft and other military platforms outside Atlanta for decades, and Gulfstream has produced world-class business jets in Savannah since the late 1950s.

More recently, Boeing’s arrival in Charleston and Airbus’s aircraft assembly facility in Mobile have added substantial scale to the region’s aviation base, drawing in suppliers, engineering talent, and research and development activity. When combined with established aerospace hubs in Huntsville and Florida’s Space Coast, these investments form a powerful, integrated industrial network that spans the full aerospace value chain. Supported by deep engineering talent, sustained federal procurement, and specialized supplier ecosystems, the sector now encompasses commercial aviation, defense systems, propulsion, composites, satellites, and space-launch platforms.

The Piedmont Triad in North Carolina exemplifies this momentum. JetZero’s roughly $4 billion blended-wing-body aircraft manufacturing hub at Piedmont Triad International Airport, announced in 2025, is projected to support more than 14,500 jobs over the life of the project, making it the largest economic development commitment in state history. Production is expected to ramp in the early-to-mid-2030s, with employment building over subsequent decades. The investment complements Boom Supersonic’s Overture Superfactory and HondaJet’s long-established and expanding operations in Greensboro, adding another major node to the South’s aerospace sector alongside Boeing in Charleston, Airbus in Mobile, GE Aerospace near Asheville, and Lockheed Martin’s F-16 production in Greenville.

Defense contracting, particularly in missiles, unmanned systems, shipbuilding, and cybersecurity, has become an increasingly important growth driver amid persistent geopolitical tensions. The sector’s wage profile is lifting incomes across Texas, Mississippi, Georgia, and Florida, reinforcing upward mobility along the value chain and supporting durable regional growth.

The space economy is also accelerating. Huntsville continues to benefit from its central role in NASA’s Artemis program and the presence of U.S. Space Command. At the same time, Florida’s Space Coast, anchored by Cape Canaveral and an expanding mix of public and private launch providers, remains a powerful engine of both civilian and military aerospace activity.

Ports, Inland Ports, and Logistics: The Quiet Force Multiplier

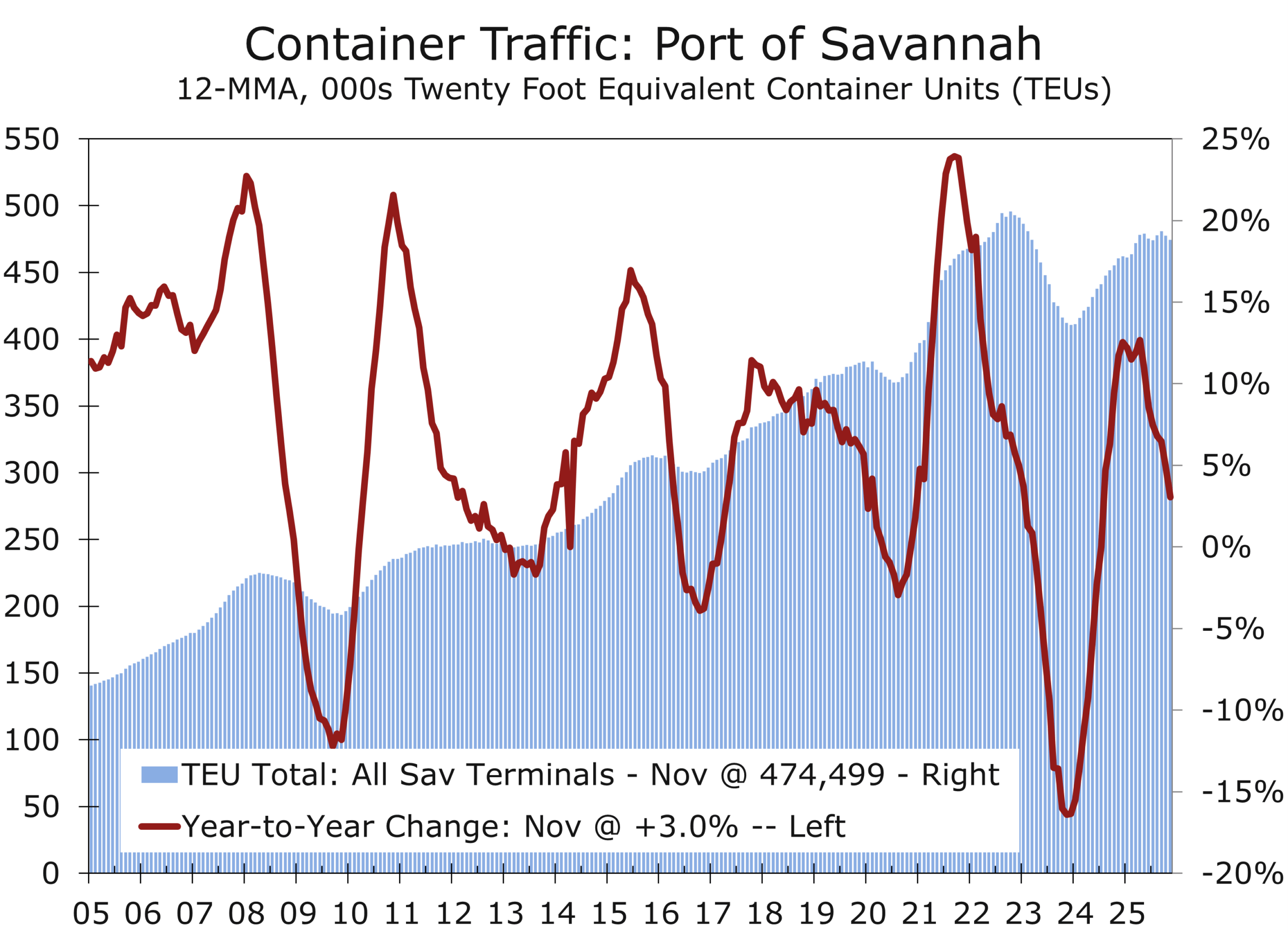

Modern logistics binds the Third Industrial Revolution, with the Port of Savannah as a prime example. Once a regional gateway, it’s now a continental platform, scaling volume through rail-centric expansions at the Garden City Terminal—the Western Hemisphere’s largest single-terminal facility. On-dock rail extends its reach inland, supporting just-in-time production and high-value exports.

Inland ports amplify this: Northwest Georgia’s Appalachian Regional Port sustains the carpet industry in Dalton and bolsters the automotive sector in Alabama and Chattanooga; South Carolina’s Greer port serves BMW, Michelin, Adidas and others; while the Carolina Connector offers daily service between Savannah and Rocky Mount, North Carolina, helping drive growth in that region. The Blue Ridge Connector, a new inland port taking shape in Northeast Georgia, will help bolster transportation links with this key poultry-producing area and support the region’s growing array of higher-value manufacturers.

The latest industrial transformation sweeping the South transcends the traditional Sunbelt narrative. The South is no longer following a low-cost growth model, but rather a capability-driven one. It reflects a fundamental reorganization of industrial, logistical, and research frameworks: merging electrification, aerospace, AI, life sciences, advanced materials, logistics, and defense into a resilient, forward-looking ecosystem.

From first in flight to the future of flight, the Southeast is setting the pace for America’s next industrial era.

Projects such as Boom Supersonic and JetZero hub in the Piedmont Triad, BMW expansion in Greenville, Boeing’s expansion in Charleston and biomanufacturing expansion in Eastern North Carolina and across the region illustrate how targeted investment builds on regional strengths to create high-wage jobs and durable innovation clusters.

Looking ahead, this integrated model positions the Southeast not only as the nation’s growth engine, but as a global leader in technology-driven, sustainable prosperity. With continued migration, retiree inflows, and capital attraction, the region is poised to drive U.S. competitiveness amid reshoring, electrification, and geopolitical realignment that will last well beyond this cycle.

January 4, 2026

Mark Vitner, Chief Economist

Southeast Economic Advisors

704-458-4000